Rightmove's slowing growth: same problem as Zillow, different strategy

/Rightmove, the U.K.'s top portal, announced its full-year 2018 results last week.

Why it matters: Not unlike Zillow, the growth in Rightmove's core advertising business continues to slow. The slowdown in velocity reveals the limits and highlights the challenges the business will need to overcome as it looks for new growth opportunities.

Overall revenue grows and slows

Overall revenue at Rightmove grew 10 percent last year -- respectable, double-digit growth, but also the lowest number recorded in its history.

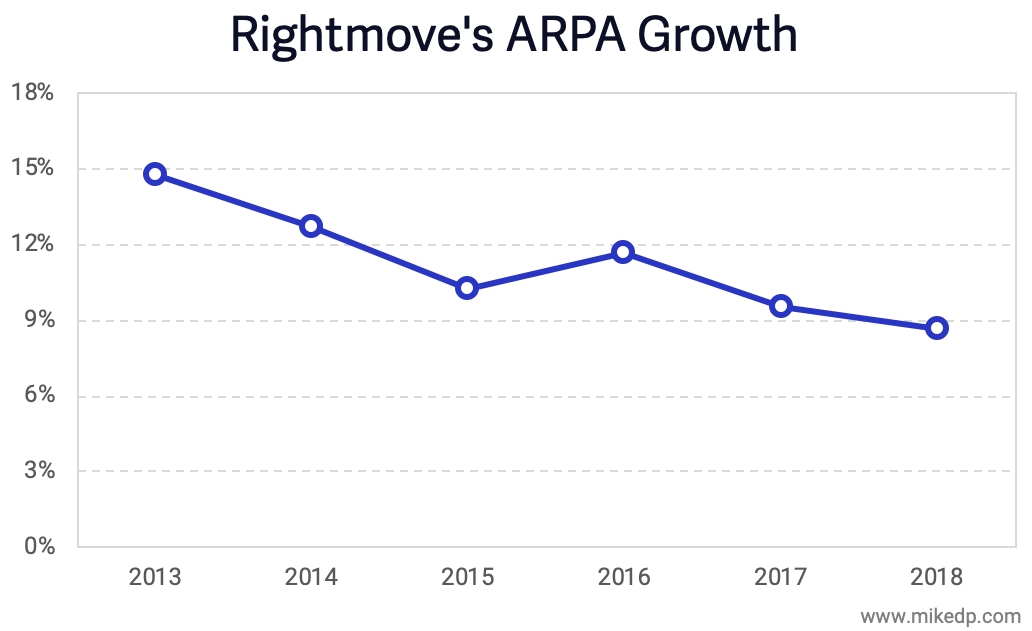

Rightmove's core revenue driver is its Agency business, which accounts for over 75 percent of total revenue (concentration risk!). Annual growth continues to slide over time. The 8.7 percent growth is the lowest number recorded, and reflects the growing difficulty the business has in charging its customers more money for the same service.

Nearly all of Rightmove's growth is coming from price increases (average revenue per advertiser, or ARPA), as opposed to new customers. The amount that Rightmove is able to squeeze out of its existing customers is slowing over time.

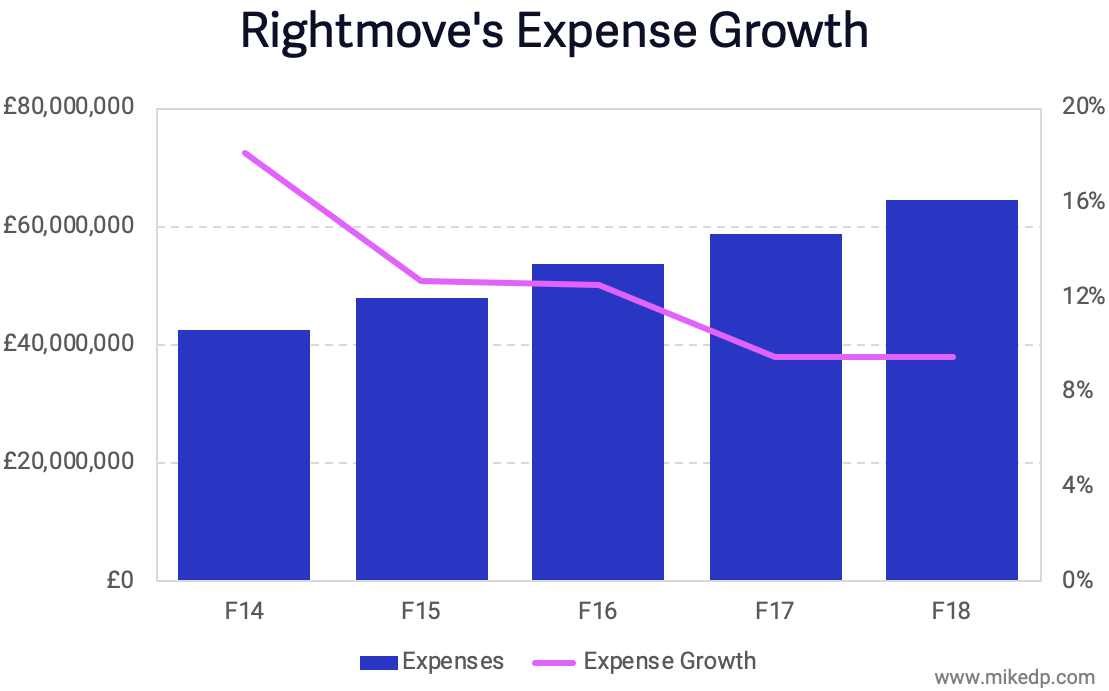

Controlling expenses

Historically, Rightmove has demonstrated incredibly disciplined cost control. By managing its expenses, Rightmove is able to maintain its phenomenal 76 percent profit margins.

But while good for the bottom line, controlling expenses too much can limit the ability of a business to invest in future revenue streams.

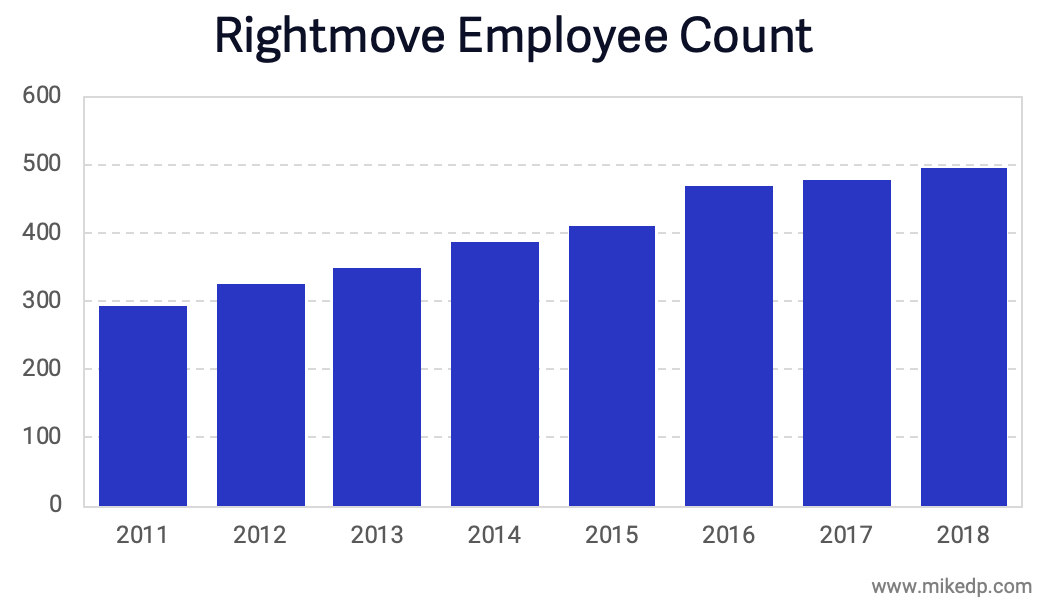

One way Rightmove maintains its margins is limited headcount growth. In 2017 (which was a transition year when revenue growth slowed considerably as new pricing was rolled out), the business only added ten new hires. In 2018, Rightmove added sixteen new hires.

Strategic implications

While facing similar challenges, Rightmove's strategy stands in stark contrast to nearly every other major real estate portal around the globe. Zillow and REA Group spent tens-of-millions of dollars to acquire mortgage businesses, Scout24 acquired a finance comparison business for over $300 million, realtor.com acquired Opcity for $210 million, and Zoopla acquired a range of adjacent businesses for half-a-billion pounds.

The real estate portal business is evolving, moving closer to and getting involved in more parts of the transaction. But Rightmove has remained steadfast and stationary in its solitary focus (more on this in my Future of Real Estate Portals Report and 2018 Global Real Estate Portal Report).

Rightmove's revenue growth slowdown may sound similar to Zillow (as I wrote about last week), although the slowdown is less pronounced and immediate. But the trend and concern is the same.

Both portals are facing slowing growth in their core businesses. Zillow has invested heavily in new business lines (mortgage, rentals, Zillow Offers, and lead qualification to name a few) and appointed a new CEO, while Rightmove hasn't -- its eggs are still in the same basket.

Zillow's New Strategy: Insights, Implications, and Analysis

/Last week, Zillow announced a major strategic shift: Along with a new CEO, it made clear that its top focus is its Zillow Offers iBuyer business.

Today's email covers the highlights of that announcement. Additionally, next week I'll be holding a 60-minute webinar that dives deep into the strategy, numbers, and implications of Zillow's latest move.

Premier agent growth grinds to a halt

The most striking statistic from Zillow's results is the lack of projected growth in its flagship, billion-dollar premier agent program (which accounts for 67 percent of its revenue). Guidance for the first quarter of 2019 is only 1.5 percent -- a steep decline from past quarters.

And on a full-year basis, Zillow projects its premier agent program will grow at 2 percent -- a flattening from past, double-digit growth.

Both of these projections come on the back of difficulties rolling out new premier agent products focused on lead quality over quantity.

But what's most striking is the suddenness of the decline. Going from double-digit to flat growth in the span of a year is significant. More than rollout issues, I believe Zillow has reached the upper limit of what it can charge agents for leads. Which is what's driving such a significant shift in strategy.

Expensive homes and a longer hold time

Last week I wrote about Zillow's unsold inventory in its Offers program, and the significance of longer hold times. The latest data highlights the same challenge.

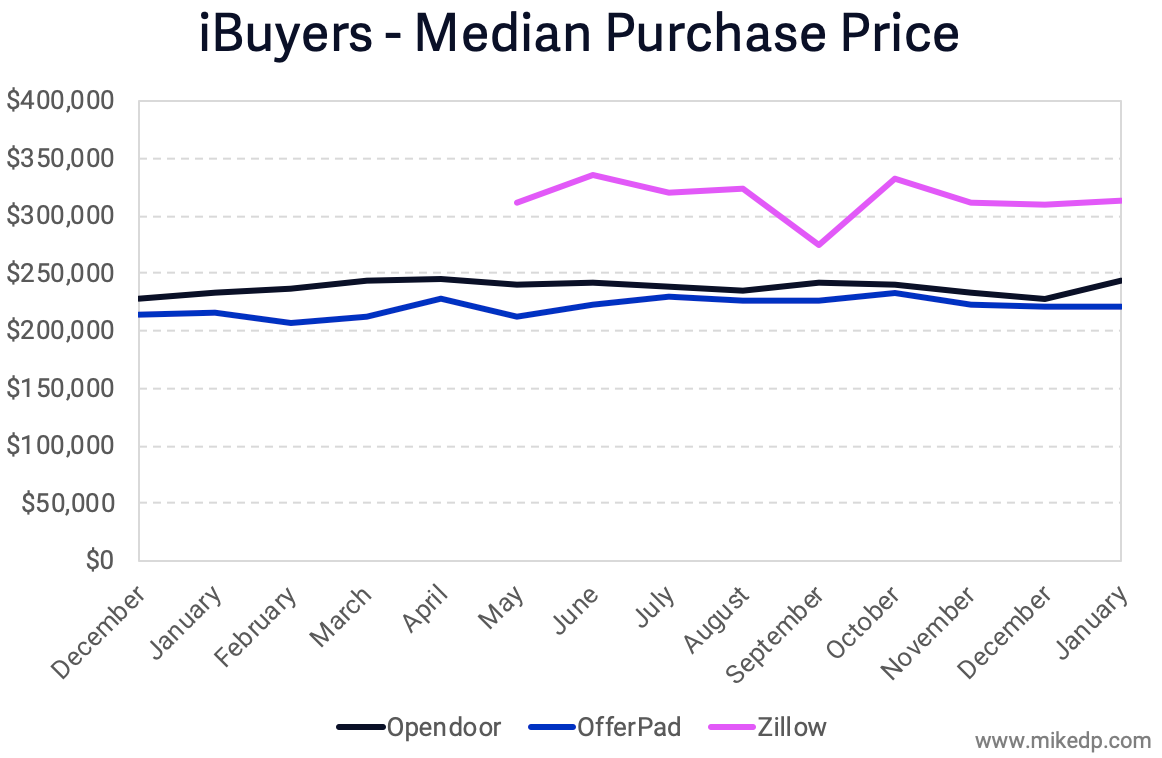

The homes Zillow sells are less expensive: an average sale price of $292,000. However, the houses it holds in inventory are considerable more expensive, with an average value of $320,000.

This data point matches up exactly with the latest data from Phoenix, which shows a considerably higher average purchase price for Zillow compared to the other iBuyers.

The more expensive the home, the higher proportion of unsold inventory. It takes longer to sell more expensive homes, and it looks like Zillow is more than dabbling in the expensive end of the market. This is a key metric to watch!

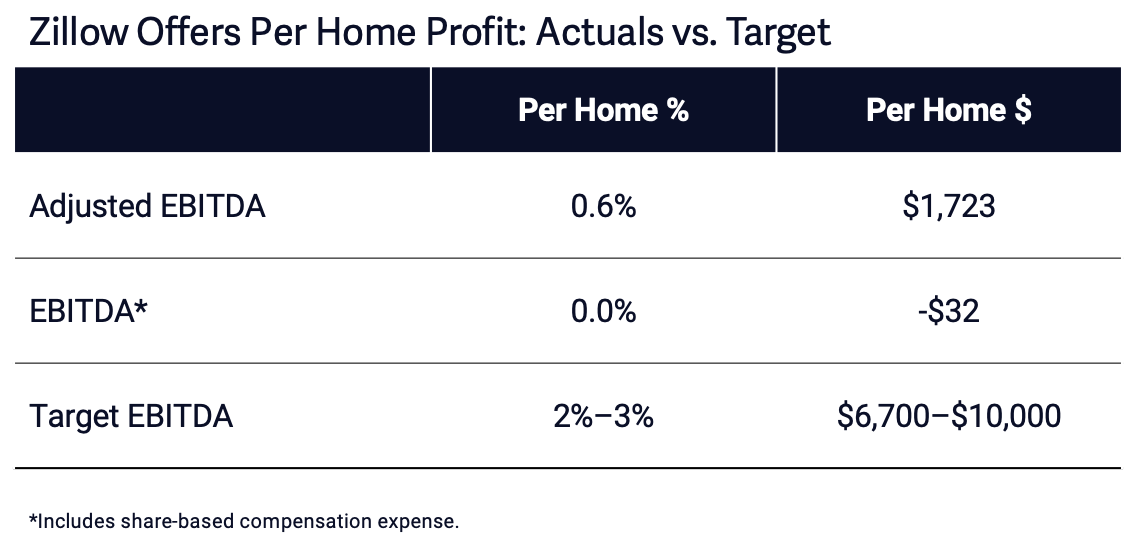

Profit projections

Zillow released a detailed financial breakdown for its Offers business, including initial profit margins on its sold homes. Adjusted EBITDA, which backs out a number of costs including stock-based compensation, shows a per-home profit margin of 0.6 percent, lower than the stated goal of 2–3 percent.

(As a form of employee compensation, I believe stock-based compensation should be included in a true EBITDA calculation, so I've provided both options above.)

It's still early days, but this benchmarks current performance compared to where the business needs and wants to go in the future.

Strategic implications

I believe Zillow's guiding strategic principle is that it must be consumers' first destination in the home buying and selling process. Zillow's sustainable competitive advantage lies in its massive audience and strong position at the start of the consumer journey.

Think of this latest move as "Zestimate 2.0." The original Zestimate gave consumers a fun and helpful starting point when thinking about moving or buying a house. Now that online valuations are a commodity, Zillow needs to up the game: Instead of an estimate of value, how about an actual offer on your house? It's a compelling consumer proposition -- even if it simply serves the same purpose as the original Zestimate (attracting consumers at the start of the journey).

There's a whole lot more to discuss! If you want to listen and watch as I dive deep into the subject, register for next week's webinar.

Zillow Offers' most important metric

/

Later today, Zillow will announce its fourth quarter and full year 2018 results. Its activity as an iBuyer continues, and it recently overtook Offerpad to become the second-largest iBuyer in Phoenix. But my attention is focused on one key metric: Zillow's ability to quickly sell houses.

Why it matters: Zillow's goal is to hold houses for an average of 90 days. Any successful iBuyer needs to hold houses for as little time as possible, otherwise unsold inventory builds up, finance costs rise, and the whole model starts to blow up.

Overall activity grows; #2 in Phoenix

Zillow's overall iBuyer activity continues to grow, both nationally and in Phoenix (its biggest market). Based on the total number of homes purchased and sold, Zillow overtook Offerpad to claim the #2 spot in Phoenix for the month of January. Zillow is -- for the moment -- the second-largest iBuyer in the important Phoenix market.

Buying more than it's selling

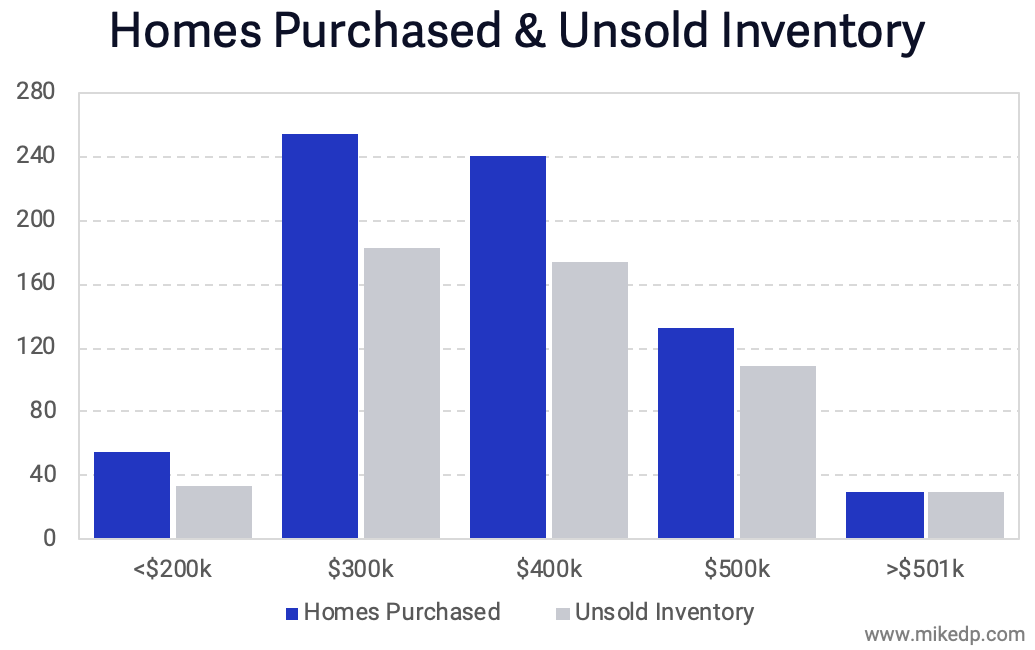

While Zillow's overall activity continues to rise, its purchases are quickly outpacing sales. This is to be expected in the early months of a new market, but it's now eight months since launch. This is creating a growing inventory of unsold homes: around 350 in Phoenix as of February 12th.

It's natural for iBuyers to buy more houses than they sell when entering a new market. But over time, this Buy:Sell ratio is a critical metric for any iBuyer. Houses must be sold for the business to work!

Expensive homes, longer hold time

There are early signs that Zillow may be having difficulty selling houses. For iBuyers, time is money. The faster they can turn around and sell a house, the better.

The magic number for total holding time is around three months; Opendoor and Offerpad hold for between 80-100 days. Zillow currently has around 350 unsold houses in its inventory in Phoenix. Of those, it appears that around 110 homes have been owned for more than three months.

Part of the reason Zillow appears to have longer holding times may be the price of the homes it is purchasing. On average, it is buying more expensive homes than the other iBuyers in Phoenix.

Nationally, Zillow has purchased over 700 homes with an unsold inventory of over 500 homes.

The more expensive the home, the higher proportion of unsold inventory. It takes longer to sell more expensive homes, and it looks like Zillow is more than dabbling in the expensive end of the market.

Strategic implications

The key metric to watch is how well Zillow can sell its houses. Buying is relatively straight-forward; only once a house is sold is the entire business model complete.

To succeed as an iBuyer and appropriately manage its risk, Zillow needs to hold its houses for a minimum amount of time (on par with the other iBuyers), and avoid building up a large inventory of unsold homes.

It's still early days and Zillow has been quite aggressive in growing as fast as possible. But with its one year anniversary four months away, the pressure is on to demonstrate a consistent ability to buy -- and sell -- houses.

My Inman Connect Presentation

/

Earlier this month I had the pleasure of presenting at Inman Connect in New York City. My session, "iBuying Goes Mainstream: How Big Can it Get?" covered a range of topics, from the evolving role of portals to the latest iBuyer analysis.

My key points are outlined below. Watch the video of my presentation and download a copy of my presentation slides.

Growing iBuyer traction

The rise of iBuyers continues. During my presentation, I shared some of the latest national data available; a "sneak peak" at my upcoming iBuyer Report.

Opendoor in particular continues its strong growth in terms of houses bought and sold, clearly accelerating in 2018. Overall, iBuyers are small but growing: around 5 percent of the market in Phoenix.

The consumer journey

If you're an Inman subscriber, you can read the provocatively titled writeup of my presentation, "Opendoor's 'nightmare': KW agents backed by their own iBuyer." To quote:

His point is that Opendoor, a tech-powered homebuying and selling startup with $1 billion in venture capital, is vulnerable to competition from companies that already connect with consumers on a massive scale at the beginning of their home-buying or selling journey.

Who wins?

The best new business models are exponentially better than the status quo, and the biggest companies are exponentially outspending their competitors.

Whether it's materially better efficiency with models like Redfin and Purplebricks, or Opendoor raising (and spending) 10 times the capital than its nearest competitors, the stakes are big. The trends that are impacting the industry are not incremental.

My presentation

You can watch the video of my presentation, and download a copy of my my presentation slides. I'd love to hear your feedback!

REA Group, Domain, and the non-battle for top spot

/It's earnings season! In the past week, a number of portals announced their financial results, including REA Group and Domain, the two top Australian portals.

Why it matters: The numbers reveal interesting trends and insights, significantly around the difficulty of building meaningful adjacent businesses, and the non-battle between the #1 and #2 players in various markets.

Adjacent businesses are tough

Like many portals worldwide, REA Group and Domain each launched adjacent businesses, with goals to expand along more of the transaction, reduce consumer friction, and capture more revenue.

But as I've written before, the businesses have very different strategies. REA Group acquired a majority stake in an existing mortgage broking business, while Domain launched a number of joint ventures and partnerships. Different strategies, different outcomes.

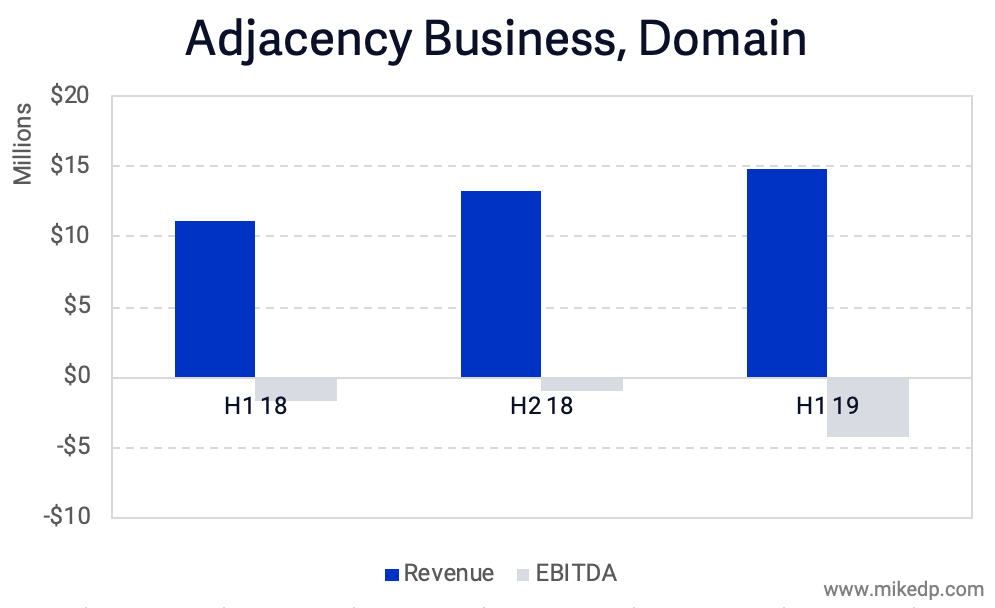

REA's finance business continues to chug along, building revenue and generating meaningful earnings ($5.8 million EBITDA over the last six months).

By comparison, Domain's adjacent businesses (finance, insurance, and utility switching) generate similar revenues but with continued -- and mounting -- losses. The latest six months show a loss of $4.3 million.

REA's strategy is delivering a positive financial impact, while Domain's businesses are still in a heavy investment phase after more than a year.

The "battle" between #1 and #2

The battle between the #1 and #2 portal in each market is fascinating, and Australia is no exception.

One metric to compare portals is overall revenue generation. In general, the #2 portal generates between 25 and 40 percent the revenue of the leader (read my portal report), and that number doesn't fluctuate over time. In fact, in the case of REA Group and Domain, the leader is growing faster than the number two.

Domain is the underdog in Australia, and the evidence suggests it will remain that way. Overall situational awareness is important: It would be a mistake to assume Domain will overtake REA in any capacity.

U.K. portal wars -- what's changing?

Along the same lines, the real estate portals in the U.K. recently released traffic figures for the start of the year. It offers yet another fascinating glimpse into the competitive tension between top players -- and the complete lack of movement.

The figures released are for January 2019. And while the absolute numbers are generally rubbish, it's the comparison between portals and the year-on-year growth that's insightful.

Rightmove's numbers have hardly changed, and the delta between the number one and two is still the same. For all the investment on product, marketing, and inventory -- the all important consumer habits haven't shifted.

The variable, however, is the upstart portal OnTheMarket (read my past analysis). OTM has raised over £30m and is aggressively spending on marketing in order to drive traffic to its site. Its traffic has doubled since last year -- but does it matter?

For all of the tens-of-millions of pounds spent to build an alternative to the established portals, what impact is it having after launching four years ago? Zoopla's traffic is marginally down, but it reports that leads are up over 30 percent. The top two portals are equally and exactly as dominant as they were a year ago.

Strategic implications

There are a number of key takeaways for portals around the world:

Launching successful adjacent businesses is hard. It takes an incredible amount of investment, and there are a variety of execution strategies.

The evidence doesn't suggest that the #2 portal can overtake the leader -- let alone make a dent in its leadership position. It's not a horse race; it's static trench warfare.

Trying to launch a new portal and compete against the leaders is at best expensive, and at worst futile. Consumer habits are hard to change.

Zoopla's private equity strategy shift

/Zoopla recently announced that it has removed all non-property advertising from its listing pages. This is one of several significant strategy changes after its acquisition by private equity firm Silver Lake.

Why it matters: The benefit of being a private company is that Zoopla can be more aggressive, focus on longer-term opportunities, and be less sensitive to a stock price that focuses on short-term earnings growth. This move is an example of that strategy in action.

The advertising revenue dilemma

A number of real estate portals generate revenue from non-property advertising on their listing pages. Zoopla's move puts it in line with arch-rival Rightmove by banishing banner ads from listing pages.

Note: REA Group and Domain do not have advertising on featured property listings, but do have non-property advertising on "normal" listings.

Banner advertising can be an important source of revenue for portals. However, it comes at the expense of the user experience. If a visitor clicks on a banner ad, their attention is diverted away from the property listing, reducing its effectiveness.

Often times user experience loses out to finances, especially for publicly listed companies under pressure to deliver revenue growth. And given that core revenue growth is slowing at a number of mature portals, the decision is even harder. But for a private company that's focused on the long-term opportunity, the decision is easy.

A shift in strategy

Aside from jettisoning nearly its entire management team, Zoopla has been up to quite a bit post-acquisition; there is the appearance of a significant change in strategy.

Zoopla's aggressive diversification strategy has been a leading factor making it unique in the world of real estate portals. It's been a world leader in acquiring adjacent businesses to dramatically grow revenues (for more on this, check out my 2018 Global Real Estate Portal Report).

The company's narrative has centered around a cross-sell strategy, where acquisitions are deeply integrated across Zoopla's network of web properties.

I've questioned the effectiveness of the cross-sell strategy, most recently in my Future of Real Estate Portals Report. The evidence didn't suggest a runaway success when it came to integration and cross-sell synergies.

Notably (and here's the big strategy shift), Zoopla's new managing director recently stated that, "Going forward, the former comparison and property businesses of ZPG will be managed largely separately, but we will continue to achieve synergies between the two wherever it is appropriate and relevant.”

To me, that sounds like a "back to basics" approach with a deep focus on the core product: tools for agents with a fantastic consumer experience. Cross-sell synergies and deep integration across the portfolio are taking a backseat.

Which is an interesting development for Scout24, which recently purchased financial comparison site Finanzcheck for $330 million, and Domain, which has been running the Zoopla diversification playbook for some time. Oops?

Strategic implications

Public companies that are focused on short-term revenue growth are at a distinct disadvantage to private companies backed by private equity. And private equity is getting more involved in the sector:

General Atlantic acquires a majority stake in Hemnet, December 2016.

Silver Lake acquires Zoopla for £2.2 billion, May 2018.

General Atlantic invests $120 million in Property Finder, November 2018.

Apax Partners offers $2.5 billion NZD for Trade Me, December 2018.

Rumors circulate that several private equity firms are looking at Germany's top portal, Scout24.

It's going to be difficult to compete with private equity-backed portals given their fundamental advantage: they can be more aggressive, focus on longer-term opportunities, and be less sensitive to a stock price that focuses on short-term earnings growth.

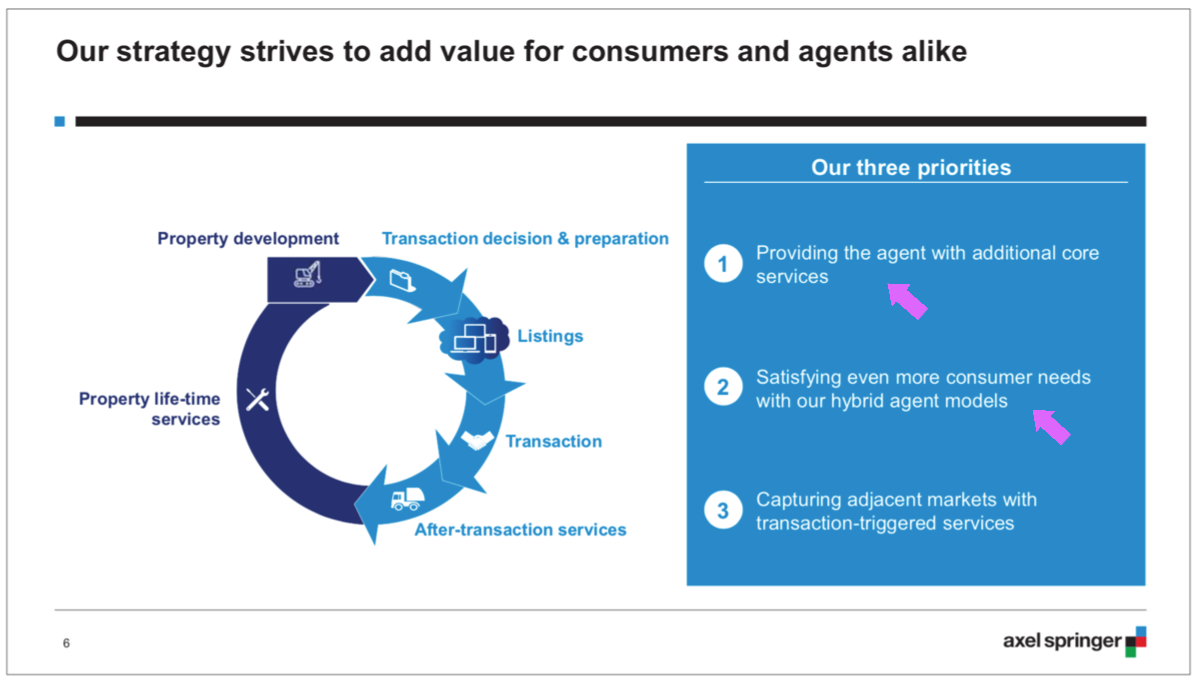

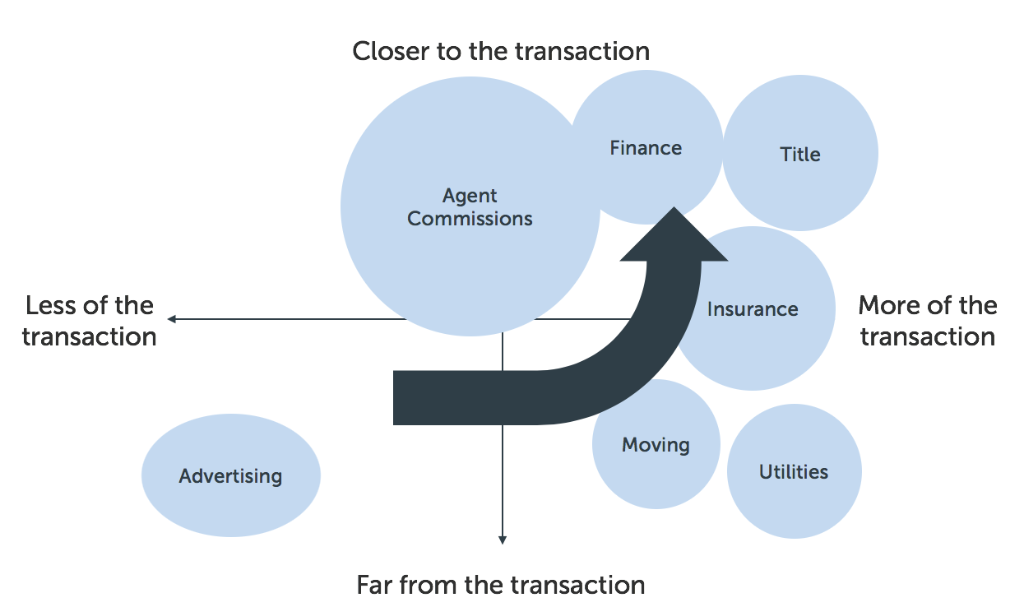

Axel Springer goes all in on hybrid agents

/How many international media conglomerates -- that own a number of leading real estate portals worldwide -- have “hybrid agents” as one of its top strategic priorities? Just one: Axel Springer.

Why it matters: Axel Springer, the $6 billion European media house, is going "all in" with online hybrid agents, through its investments in Purplebricks and Homeday. It's making a calculated bet that competing with its real estate agency customers is the best long-term strategy.

Making hybrid agents a strategic priority

Dozens of the largest real estate portals around the world are owned by a small collection of international media companies: News Corp, Schibsted, Naspers, and Axel Springer. But of them all, only Axel Springer has taken the step of investing in a potential sector disruptor: the online hybrid agent.

Axel Springer owns major real estate portals in France, Germany, Belgium, and Israel. In March 2018, it made a bold, £125 million investment in Purplebricks. The investment is notable because Axel Springer owns several top portals whose customers are the same real estate agents that Purplebricks is trying to disrupt (albeit in different markets).

Furthermore, Axel Springer is the only major international entity that has targeted online hybrid agents as a future growth priority. In its latest presentation to investors, hybrid agents are included as a top priority for the core classifieds business (which generated revenues of over €500 million in 2017).

Disrupting its biggest customers

Axel Springer's strategy offers a fascinating juxtaposition: Adding value to traditional agents by providing more services (seller leads), while "satisfying even more consumer needs" with its hybrid agents -- which directly compete with traditional agents.

Axel Springer is wonderfully upfront about its motivations. Its move into the hybrid agent space is designed to tap into a much larger revenue pool: agent commissions.

Continuing to serve your customers while entering into direct competition with them is a delicate balancing act. It's a move reminiscent of Amazon promoting its own products in direct competition with many of its sellers.

This is the nightmare scenario that U.S. real estate agents have been predicting for years. But in this instance it's not Zillow, but one of Europe's most powerful players, taking active steps to disrupt agents.

Winner take most

It's been clearly illustrated in the U.K. market that the online agent space is winner take most (market share). Access to capital is the single biggest predictor of success.

There is no first mover advantage in these markets (Purplebricks was not the U.K.'s first online hybrid agent). Rather, there is a rich first mover advantage: the business with the deepest pockets generally wins.

In this regard, Axel Springer and Purplebricks form a powerful combination. From a competitive standpoint, the most dangerous thing about Purplebricks is its investment risk tolerance. It is willing to invest tens-of-millions of dollars year after year to build market share -- incurring big losses along the way. And with Axel Springer and its deep pockets along for the journey, it's a hard combination to beat.

Strategic implications

Axel Springer and Purplebricks are quickly building a potentially insurmountable lead in the online hybrid agent space globally. There is no runner-up in the sector; it's a one horse race.

Purplebricks has proven the online hybrid model works in the U.K., and is aggressively launching in other markets. Copycats are popping up around the world. What's stopping News Corp, Schibsted, and Naspers from entering the space? It's either capital, ambition, or fear of upsetting their agent customers.

Real estate portals are moving from search engine to service engine; they are moving closer to and becoming involved in more of the transaction.

There is undeniable momentum in this direction. While not every portal is seeing success, the shift is clear -- and unyielding. Axel Springer's bet on online hybrid agents, in direct competition with its real estate agent customers, is the latest example of this evolving strategy.

2018 in Review

/

What a year! In 2018, I published a massive amount of insightful, data-driven analysis of the global real estate tech landscape, and started as a scholar-in-residence at the University of Colorado Boulder. I'll cover the highlights below, but first a look ahead.

Themes for 2019

Next year, my work will focus on three main areas:

Big real estate portals aggressively launching new revenue streams in adjacent businesses, moving from search engine to service engine.

New models continuing to gain traction, with accelerated expansion in mature markets and start-ups launching everywhere else.

Traditional real estate incumbents around the world taking note and reacting -- some better than others.

2018 Highlights

Three huge reports

I released three reports: the 2018 Emerging Models in Real Estate Report (33k views), the 2018 Global Real Estate Portal Report, and the Future of Real Estate Portals.

Zillow and iBuyers

I conducted a deep analysis of Zillow's strategic shift, how Zillow and Opendoor are controlling the consumer journey, and the billion dollar seller lead opportunity.

Disruptive new models

Looking broader, I asked if Compass really is a tech company, and

analyzed online agent consolidation in the U.K. and how psychology is holding back real estate tech.

Strategy consulting

I've worked exclusively with the world's leading and most promising real estate tech companies and portals (you know who you are, and thank you), conducting strategy reviews and ongoing advisory work.

Keynote presentations

From San Francisco to Oslo, Dubai to Berlin, I've delivered top-notch insights in person to the biggest companies and leaders in the field. Read some testimonials.

University course

I started teaching real estate tech at CU Boulder, with amazing industry guest speakers from companies like Trulia, Opendoor, UDR, Open Listings, ATTOM Data, and more.

Investments in real estate tech

During the course of 2018, it's been my pleasure to join world class investors like Axel Springer, Kleiner Perkins, Stereo Capital, Lightspeed Ventures, Breyer Capital, and Schibsted Media as a personal investor in or advisor to real estate tech companies Zumper, Fastfox, Kodit.io, Tall Poppy, and AirDNA.

An exciting year ahead

I'm looking forward to exploring new opportunities and applying my expertise to new challenges in the year ahead. I'll drive myself to continue to be -- in the words of one of my readers -- "the most reliable source for data-driven, strategic insights in the industry."

My Proptech CEO Summit Presentation

/

It was my pleasure to present at the invite-only Proptech CEO Summit in San Francisco, hosted by former Trulia execs and current venture capitalists, Paul Levine and Pete Flint. There were over 100 proptech CEOs present, including Glenn from Redfin, Eric from Opendoor, and many others.

I want to share my entire presentation from the event, in addition to highlighting a few key points.

PropTech and PropPsych

The first point deals with the critical role of human psychology in real estate transactions, and the concept of loss aversion (for more, check out How Psychology is Holding Back Real Estate Tech).

Human psychology is the single biggest obstacle to mainstream adoption of new technologies in real estate. The point I made in my presentation is this: every venture capitalist should be asking proptech start-ups how they are going to address loss aversion.

And the inverse is true: each startup should clearly explain how its product or service is designed to minimize loss aversion in consumers.

Building the technology alone is not enough. Real estate tech companies need to assure consumers their product is just as "safe" as the status quo. PropPsych is just as important as PropTech.

Solving problems with money

The second point relates to the massive amounts of money flowing into the ecosystem. To quote Glenn Kelman, "If we can afford to lose money for five years, how can we ever make money?"

The biggest players in the space -- Opendoor, Purplebricks, and Compass -- have raised hundreds of millions to over a billion dollars each. The next tier of start-ups have raised tens of millions of dollars each.

But none of these companies are actually doing something new; they're doing what's possible with massive amounts of capital.

Yes, there are novel aspects of the business models that allow these business to realize gains in efficiency, or provide a superior customer experience. But all are underpinned by massive amounts of capital.

The reason that Compass can buy market share, Purplebricks can generate tons of leads through advertising, and Opendoor can buy thousands of homes is access to vast amounts of capital.

My presentation

Attached below is a link to my presentation on Slideshare (you can also download the PDF). Unlike my numerous industry reports, this is designed to be delivered in person. But hopefully it helps you and your business.

Purplebricks' H1 2019 Results

/Last week, Purplebricks released its half-year financial results. The top line results include an overall group loss of £27.3 million for the period, with a slight reduction of its full-year revenue guidance. But the top line numbers don't come close to telling the full story (hint: it's not as bad as it sounds).

Why it matters: Purplebricks' core U.K. market continues to grow and is meaningfully profitable, proving that the model works. Key performance indicators in its other three markets reveal a deeper story of investment, growth, and challenges.

Continued growth in the U.K.

The popular narrative is seductive, but factually incorrect: With massive losses at Purplebricks and the demise of online agent Emoov (which, by the way, was not the second largest online agent in the U.K.), the entire online agency business model is near collapse. Not quite.

Purplebricks is an international collection of businesses at various stages of growth. In the U.K., Purplebricks' most mature market, it continues to grow revenues and operating profit. At maturity and scale the business model absolutely works; there is no evidence to support otherwise.

Yes, growth is slowing in the U.K. But at nearly 80,000 instructions per year it can't be expected to keep growing at historic rates. The key is that even in a challenging economic climate, growth continues.

Bumpy ride in Australia

While progress in the U.K. is consistent and positive, Purplebricks' Australian operation has endured a turbulent year. Senior management changes, a business model pivot, and its fair share of negative press has resulted in a "bump in the road" over the last six months.

Revenue growth is up year-on-year, but down from the previous six months, with a corresponding hit in operating profit.

One data point does not make a trend, so all eyes are on the next six months as Purplebricks executes its Australian turnaround plan with a new team and new pricing strategy.

Deep investment in the U.S. market

Purplebricks continues to invest heavily in its U.S. rollout. Over the past six months, it has spent over $20 million on sales and marketing across seven States -- more than double what it spent last year.

Purplebricks managed between 1,200 and 1,400 instructions in the U.S. over the past half-year, or around 200-230 per month. The cost per instruction has dropped from around $21,000 to between $14,000 and $17,000 (each instruction is worth $5,205 in revenue to Purplebricks).

At the current rate, Purplebricks will need to go from 200 to 650 instructions per month to reach breakeven with its sales and marketing costs, and to 1,000 instructions per month to reach profitability.

To achieve profitability, Purplebricks will need to get all of its launch markets performing well, not just L.A. One example is the lackluster performance in Phoenix, as I wrote about last week.

Marketing efficiency

At its core, Purplebricks is as much an advertising company as it is a real estate company. The business model relies on a massive marketing expenditure to generate leads for its network of agents. Thus, one of the most important metrics for the business is marketing efficiency.

For every £1 spent on marketing, Purplebricks generates revenues of £3.60 in the U.K., £0.92 in Australia, £0.36 in the U.S., and £4.38 in Canada (Purplebricks' Canadian acquisition was a fantastic deal).

Strategic implications

The core Purplebricks business model -- and profitability at scale -- is sound. The market failure of smaller players, or the fact that Purplebricks is deeply investing in new markets, doesn't diminish that fact.

From a competitive standpoint, the most dangerous thing about Purplebricks is its investment risk tolerance. It is willing to invest tens-of-millions of dollars year after year to build market share -- incurring big losses along the way. If you're a traditional real estate agency, or a listed company, are you willing to do the same?

Trade Me's private equity adventure

/In recent weeks, Trade Me, New Zealand's leading classifieds and marketplace portal, has received two, multi-billion-dollar buy-out offers from private equity firms.

Why it matters: There is a growing trend of private equity getting involved in portals around the world, which allows these businesses more freedom of action as private companies -- but with significant change.

Private equity and portals

Trade Me is New Zealand's leading portal, with property, automotive, and jobs classifieds and a general marketplace business. I worked there as head of strategy between 2012 and 2016.

British firm Apax Partners and American firm Hellman & Friedman have both offered around $2.5 billion NZD for the business, a 25 percent premium to the existing share price.

This news follows several other examples of private equity getting into the (property) portal business:

General Atlantic acquires a majority stake in Hemnet, December 2016.

Silver Lake acquires Zoopla for £2.2 billion, May 2018.

General Atlantic invests $120 million in Property Finder, November 2018.

Slowing growth

Since its public debut eight years ago, Trade Me has grown revenues 100 percent and net profit 39 percent.

Revenue growth has slowed over the years, especially recently, in a story reminiscent of Rightmove's growth dilemma.

The stock price has seen a steady rise with its ups and downs, but has been relatively flat since 2017.

In August of 2018, Trade Me announced a special dividend to return $100 million in capital to investors. This comes on top of the normal dividend, which represents around 80 percent of profits. Returning capital at that scale can be a signal that the company has run out of ideas.

Many businesses believe it is more beneficial to reinvest profits to improve efficiency, expand reach, create new products and services as well as improve existing ones, and further separate themselves from competitors.

Like Rightmove, Trade Me is in a difficult position. With growth slowing, it is less likely to make big investments for fear of depressing earnings and upsetting investors. It's a delicate, public-company balance. Enter private equity...

Upside potential, with change

Private equity invests in businesses for one and only reason: to make money. It's clear that these P.E. firms have evaluated Trade Me's business and believe there is significant upside potential under new ownership and management.

But significant growth comes with significant change. When Silver Lake acquired Zoopla in the U.K., nearly the entire executive team was let go as part of the restructuring. It's the same story in Sweden, when General Atlantic appointed a new management team after acquiring a majority stake in Hemnet.

Strategic implications

If consummated, a private equity takeover of Trade Me would have a number of implications for the business, competitors, and the entire online ecosystem:

A private ownership structure will allow Trade Me to be more aggressive, focus on longer-term opportunities, and be less sensitive to a stock price that focuses on short-term earnings growth.

Private equity firms demand a return on their investment, and this transaction will be no exception. Expect costs to be trimmed, earnings maximized, and a more aggressive posture on pricing and monetization.

If you're competing with Trade Me, expect a dramatically different business to emerge that's tougher, less conservative, and more willing to throw its weight around.

Trade Me has long had a friendly, home-grown feel in New Zealand. New owners -- and new demands on the business -- may change the equation.

Purplebricks struggles in Phoenix

/I had high hopes when Purplebricks launched in Phoenix earlier this year. It was the first U.S. market in the "sweet spot" for the Purplebricks proposition. However, the latest numbers show quite modest traction: 75 listings and 26 sold properties over five months.

Why it matters: This data presents a healthy counter-balance to Purplebricks' rapid, national expansion. Launching in a new market is very different than gaining meaningful traction in a new market.

Mid-market America

In July, I analyzed Purplebricks' FY18 results. The analysis highlights the massive investment the business made with its U.S. launch, with an effective cost per listing of over $21,000.

There's also the question of if Purplebricks launched in the wrong markets. Southern California and the New York metro area are expensive markets, while the data clearly shows the Purplebricks proposition resonating with mid-market customers. Phoenix is that market.

After a slow start, Purplebricks is averaging a few dozen new listings per month in Phoenix. With a listing fee of $3,600, that's around $75,000 in revenue for November.

Purplebricks is also struggling to recruit and retain brokers in Phoenix. Agent numbers are stagnant, and the average number of listings per broker is two. If we assume a broker is paid $1,000 of the $3,600 listing fee, that's a very low effective annual pay package. (Broker numbers can be tracked on the Arizona Department of Real Estate web site.)

The right market

I still believe Phoenix is the right market for Purplebricks. The 75 Purplebricks listings are right in line with the median average for the Phoenix market (Maricopa County), which is a positive sign. This -- not more expensive markets -- is the sweet spot for the fixed-fee proposition.

Growth is the name of the game

The U.S. real estate market is undergoing significant change. New (and existing) players like Redfin, Compass, and eXp Realty are rapidly growing market share -- at the expense of traditional incumbents.

All of these players, including Purplebricks, have raised massive amounts of capital to grow market share. Growth is measured in tens-of-thousands of new listings.

Phoenix is just one market out of several in the U.S. where Purplebricks has launched. In its first eight months, Purplebricks had 582 total listings nationally. After five months in Phoenix, 75 total listings is a comparative drop in the bucket. If Purplebricks wants to make a dent in the U.S., these numbers need to be in the hundreds and thousands.

Another data point: A quick check on Zillow shows 288 active listings for Purplebricks (primarily in California); it had 289 back in June. By comparison, Opendoor grew from 721 to 3,163 active listings in the same period.

Strategic implications

Purplebricks' success in the U.S. market is not assured. Raising a lot of money doesn't guarantee success. And an organic pathway to growth takes large amounts of time, patience, and capital.

Execution of this model is very much market-specific, and a lot of hard work. The business model scales linearly with people; technology is just an enabler.

Zillow's billion dollar seller lead opportunity

/Last week, Zillow announced its latest financial results, and the stock dropped 25 percent (losing $2 billion in value). But the story everyone is missing is the Zillow Offers iBuying business, and the huge potential of seller leads.

Why it matters: Last week I was quoted on MarketWatch saying, “If you’re thinking about Zillow doing iBuying and you’re not thinking about seller leads, you’re thinking about it the wrong way.” Seller leads are the real billion dollar opportunity.

Slowing premier agent growth

Here's the reason why Zillow's stock tanked 25 percent last week, in one chart:

Zillow's premier agent program accounts for over 70 percent of its revenue, or nearly $1 billion. Growth is slowing down. I'm not sure why this surprised anyone on Wall Street; I've been writing about it since early this year (Zillow's revenue growth slows and Zillow's strategic shift to iBuying and mortgages). I believe it's the primary reason Zillow has aggressively expanded into adjacent businesses.

The value of seller leads

Zillow's iBuyer business continues to grow, and the latest results crystalize the opportunity in seller leads.

Zillow says that since launch, nearly 20,000 homeowners have taken direct action on its platform to sell their home. Of those, it has purchased just about 1 percent of homes (around 200). That leaves about 19,800 leads who remain interested in selling their homes.

If Zillow simply sold those leads at $100 a pop, they're worth nearly $2 million.

But the real opportunity is giving those leads to premier agents in exchange for an industry-standard referral fee, about 1 percent, if the property sells (similar to the Opcity business model).

Here's the kicker: Zillow claims about 45 percent of consumers that go through the Zillow Offers funnel end up listing their home. That's a high conversion rate reflective of a high intent to sell; about 10 times higher than Opcity's conversion rate.

Assuming a 1 percent referral fee, a $250,000 home, and a conversion rate of 45 percent, those 19,800 leads are worth $22 million in revenue to Zillow, almost all profit.

Compare that to the estimated profit of its iBuyer business (1.5 percent net profit), which, on 200 houses, is $750,000. The value of the seller leads is worth almost 30 times the profit from flipping houses!

Total addressable market

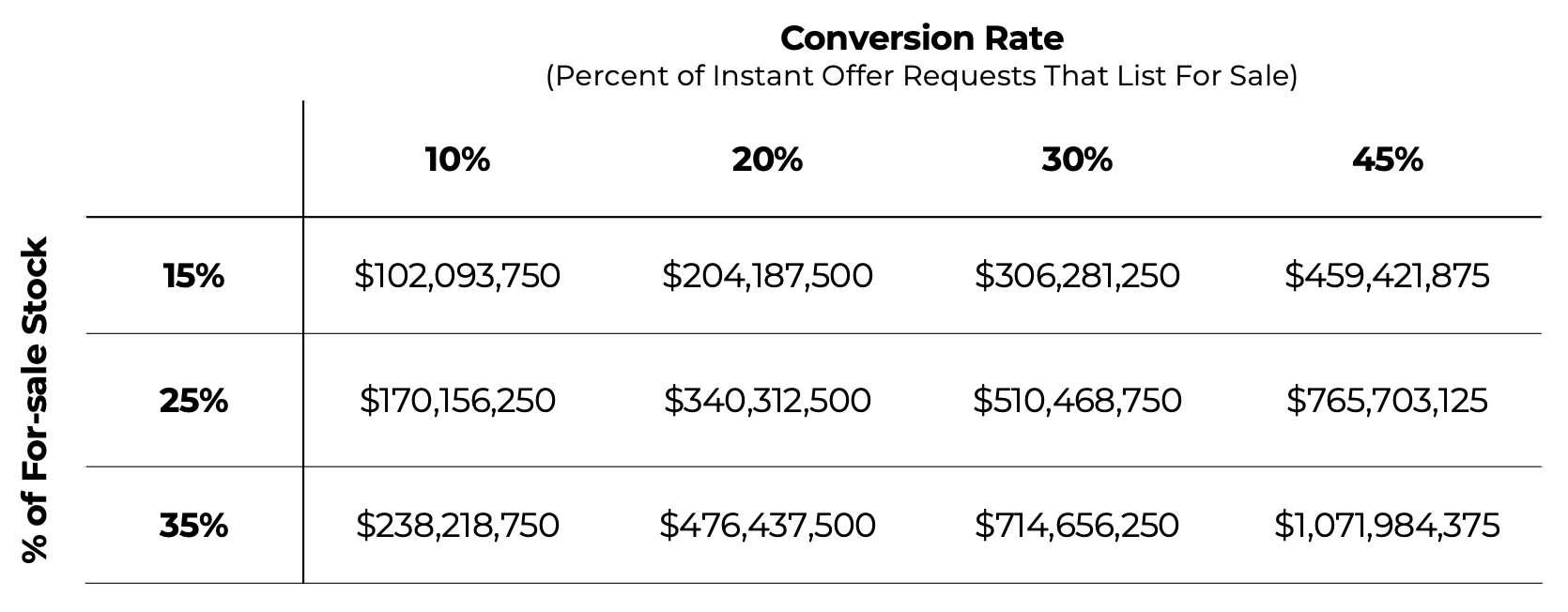

Zillow says that based on its current purchase criteria, if Zillow Offers were available in the top 200 metro areas in the U.S., sellers of nearly half of the homes sold in 2017 across the entire nation would have been eligible to receive offers from it to buy their home directly. That equates to around 2.75 million homes annually.

Last quarter, Zillow said that it received offer requests from around 15 percent of the total for-sale stock in the Phoenix market. Interestingly, that number increased to 25 percent in September and 35 percent in October. That's a reflection of the strong lead generation power of Zillow Offers across its various web properties.

Based on these numbers, if Zillow goes national (200 metro areas) and sees 35 percent of the for-sale stock, it would receive 962,500 offer requests each year.

The billion dollar opportunity

Taking the latest numbers, which have been validated to the tune of 20,000 offer requests over five months in two markets, the total opportunity becomes clear with a national rollout.

Seller leads can be a billion dollar business for Zillow if you believe the current numbers. Even if a national conversion rate is lower, or the % of for-sale stock fluctuates, it's still worth several hundred million dollars in revenue annually.

Should Zillow even buy houses?

Given the value of the seller leads, should Zillow even be in the business of buying houses? Yes, if it wants a credible product for consumers. The real question is: What proportion of houses should Zillow actually buy?

Zillow's "big picture" is 5 percent national market share, which equates to buying around 10 percent of all offer requests (it is currently buying around 1 percent of offer requests). At a 1.5 percent net margin, that's around $1 billion in profit.

But to reach that scale, Zillow would need to spend $68 billion to purchase 275,000 houses annually. Assuming an average holding time of 90 days, it would need a credit line of $17 billion to fund the effort. Big numbers.

A more realistic target would be to only purchase around 1 percent of requests. Nationally, that would be 27,500 homes, which is only around double what Opendoor is currently doing, so it's feasible.

In any case, the point is clear: Zillow doesn't need to actually buy and sell a lot of houses for this model to generate significant profits for the company in a national rollout.

Strategic implications

Zillow is a lead generation machine, and its recent foray into iBuying is no exception.

If you're in the industry and your value proposition to agents is seller lead generation, there's a new game in town. Zillow will be able to generate a massive volume of seller leads with higher intent than almost any other source. If successful, this will have significant implications across the industry.

Further analysis

If you're looking to dive deeper into the world of iBuyers, consider the following:

iBuyer Business Model Overview and Analysis: all of my free research and reports on the iBuyer space.

iBuyer Intelligence Briefing (Recording): a 60-minute conference call I conducted on the latest iBuyer news, key insights, and strategic implications for the real estate industry.

Phoenix iBuyer Report: the only source for accurate, timely iBuyer market data for Phoenix. Available as a monthly subscription.

Mobile contact form analysis

/Inspired by a recent talk on the importance of mobile experiences, I've conducted an analysis of the mobile contact forms for the big real estate portals. These are the forms that turn visitors into leads.

Why it matters: Mobile is huge. My research of the top real estate portals shows that, on average, 70 percent of leads come from mobile. Mobile contact forms should be optimized to be as efficient as possible.

Notable UX highlights

Pre-selecting checkboxes is a real-world example of behavioral science (specifically nudge theory) in action. In the U.S., Zillow and realtor.com take different approaches to encourage (or discourage) users to request additional financing information. Overseas, Propertyfinder, PropertyGuru and Otodom do the same when it comes to signing users up for property alerts.

Trade Me has the unique distinction of having the easiest and most difficult mobile form. On the positive side, it is the shortest form from my survey, simply asking for a message. On the negative side, it requires users to sign in to send a message. Luckily, almost the entire population of New Zealand is a member of Trade Me, but in the case of a new user (or someone who isn't logged in), this introduces a significant form completion hurdle.

The more required fields, the more difficult to complete a form. I know Germans can be formal at times, but does salutation really need to be a required field for ImmoScout24?

Redfin has split its form across three screens, each quite simple. But the additional effort to click a submission button three times instead of one, plus additional page load time, adds significant (and unnecessary) overhead.

Hemnet has decided to do away with forms all together and simply list an email address, leaving communication entirely in the user's hands!

Mobile usage

Many thanks to the portals that were willing to share their data with me (both anonymously and on the record). The collective intelligence is a benefit to all!

The percentage of leads that come from mobile (native app or mobile web) varies greatly: from 40 percent in Poland (Otodom) to 91 percent in Singapore (PropertyGuru).

The biggest markets average somewhere in the middle: around 65 percent in the U.K. (Zoopla) to 72 percent in Australia (Domain).

On average, around 70 percent of all leads come from a mobile device, underlining the importance of a smooth mobile user experience.

User experience best practices

Best Practices for Mobile Form Design is an incredible resource for designing simple and effective mobile forms. Looking at the mobile forms from this survey, there are several best practices to remember:

Avoid dropdown menus (dropdowns are especially bad for mobile).

Don't slice data fields (when asking for a first and last name).

Mark optional fields instead of mandatory ones (don't use asterisks).

A number of real estate portals do a great job at keeping the mobile experience simple and easy by following best practices and keeping the form as short as possible. My hope is that next year the forms will be even easier for users to complete. And if you're wondering just how important leads are, just ask Zillow.

Before entering the high-octane world of real estate tech strategy, I was a product guy. My master's degree was in human-computer interaction, and I spent the first years of my career as a user interface designer. So I'm passionate about great design!

Opendoor's pivot to agents

/According to a report on Inman, Opendoor is launching a new preferred agent partnership program where it is co-listing a growing portion of its for sale properties with partner agents.

Why it matters: This is a significant pivot for Opendoor, aligning it closer to agents in a major way. It signals that working with the traditional industry -- rather than trying to disrupt it -- is an important part of its growth strategy.

Working with agents

Opendoor's new preferred agent partnership program brings the company much closer to agents. As opposed to the company's hallmark of buying and selling direct to consumers, with a do-it-yourself open home model, this latest move represents a big pivot.

Before this program was announced, the way Opendoor sold its homes was fairly uniform: it would list direct without an agent, offer self-guided tours, brand everything Opendoor, and not pay seller agent fees since it was selling direct. But things have changed:

An unknown question is how Opendoor is compensating co-listing agents. There are three possibilities, listed in order of likelihood:

The agent receives a referral fee (likely 1 percent) for representing Opendoor.

The agent receives a fixed fee ($1,000) for representing Opendoor.

The agent receives no direct compensation, but benefits from potential leads while hosting open homes.

Why the pivot?

This is a big move for Opendoor, and it would only make a change if there was a business benefit.

Opendoor is moving towards an agent-centric model, where it's co-listing and co-branding with a traditional real estate agent (and the traditional process it is aiming to disrupt). That's a non-trivial shift. And assuming Opendoor is compensating co-listing agents as outlined above, there's a significant economic shift as well.

Opendoor is in the business of buying and selling houses. So any pivot must enhance that capability, leading to two possible reasons for the change:

Sell more houses, faster.

Attract more agents representing sellers (buy more houses).

For a co-listing arrangement to make business sense, it must enable Opendoor to buy or sell more houses. Either its existing process isn't quite where Opendoor wants it to be, or there's an external reason to cozy up to agents...

The Zillow factor

There's one other factor to consider, and that's the relatively recent arrival of Zillow to the iBuyer game. As a reminder, Zillow's angle is to include agents in each step of the process, using its premier agent network to represent all sides of the transaction.

Opendoor's latest move puts it squarely at parity with Zillow in terms of agent involvement and the value proposition for agents.

Now, if you're an agent, the benefits of working with Opendoor are the same as working with Zillow. For Opendoor to make this degree of change, and give up image and economic value in order to appeal to agents, it must really want to work with agents!

Strategic implications

There's a long history of would-be real estate disruptors that attempted to disintermediate the traditional industry, only to change their minds and pivot back.

It's hard to go against real estate agents. There's just so many of them, and psychologically consumers want to keep using them. Many disruptors start with anti-agent tendencies but eventually come back to the fold. It's easier and more profitable to work with the industry than against it.

This is not a full-scale retreat on Opendoor's part; far from it. But it's the strongest signal yet of the importance of agents to its current growth strategy.

2018 Global Real Estate Portal Report

/

Looking for more? Download and watch my Global Real Estate Portal Intelligence Briefing, a 60-minute webinar to dive deeper into the key highlights, trends, and insights from my latest report. I'll walk you through the key takeaways and observations from my research, in addition to answering questions.

Why incumbents can't beat Zillow (and the power of network effects)

/Recently, several large incumbents have announced big consumer plays aimed at Zillow: Rocket Homes' new consumer portal, and Keller Williams acquiring SmarterAgent as part of its consumer strategy.

Why it matters: Zillow benefits from practically unbeatable network effects in the consumer space. Both of these moves ignore basic strategic principles of playing to your strengths, and picking battles you can win.

Network effects and wide moats

In his best-selling book Zero to One, Peter Thiel provides an elegant definition of network effects: “Network effects makes a product more useful as more people use it. For example, if all your friends are on Facebook, it makes sense for you to join Facebook, too.”

Online marketplaces such as Craigslist, LinkedIn, and eBay are classic examples of businesses that benefit from network effects. The more people that use them -- buyers and sellers -- the more valuable the service becomes.

Businesses that have the benefit of network effects are incredibly difficult to displace. As Tren Griffin writes on a16z, "Nothing scales as well as a software business, and nothing creates a moat for that business more effectively than network effects."

Zillow benefits from the power of network effects. By developing the most popular means of searching for real estate, it attracts buyers and sellers in a virtuous cycle. It has cemented an incredibly strong position with a near-impenetrable moat from competition. This is Zillow's key strength.

Comfortably number one

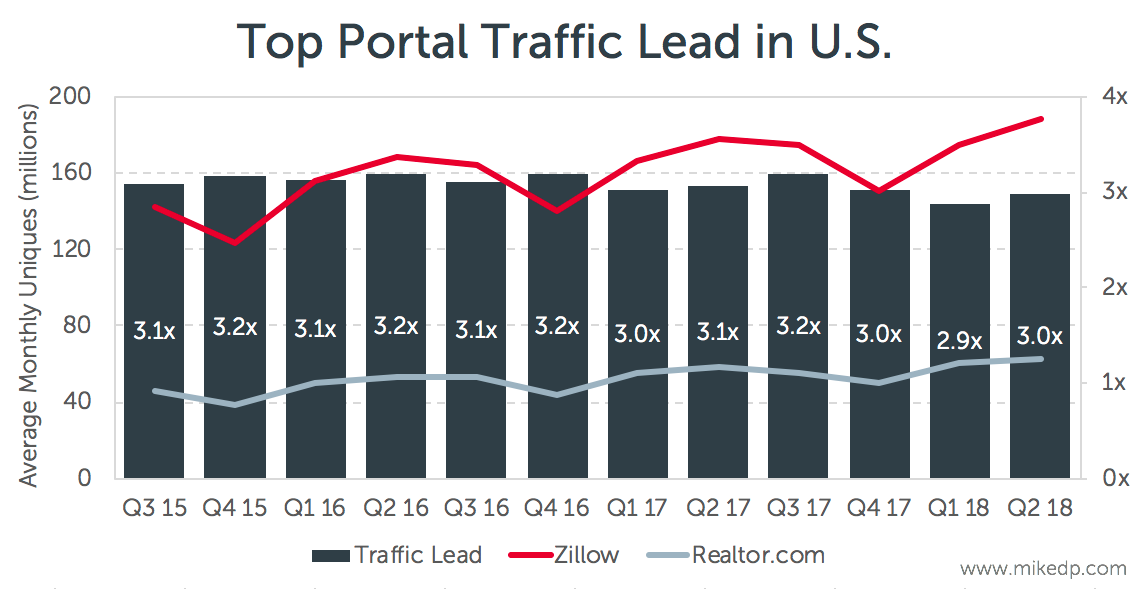

Logically, the most likely competitor to challenge Zillow's dominance is realtor.com. It is the runner-up portal backed by a multi-billion dollar international media company (News Corp) that also owns several top portals around the world.

But as I've shown in the past, Zillow's ever-important traffic dominance remains constant, undisturbed by realtor.com or anyone else.

If anyone could dislodge Zillow's dominance, it would be realtor.com. But it hasn't; not for lack of trying, but rather an understanding of network effects and the futility of such an effort (remember, it owns the top portal in Australia and knows the power of network effects better than most). News Corp doesn't want to overtake Zillow because it knows it's impossible.

Strategy basics: play to your strengths

Sound strategic planning requires two key elements: leveraging your strengths, and playing where you can win.

A business should build its strategy around an understanding of its key competitive advantages and operational strengths. Those strengths should be applied in areas where it can win (typically where its competitors are weak).

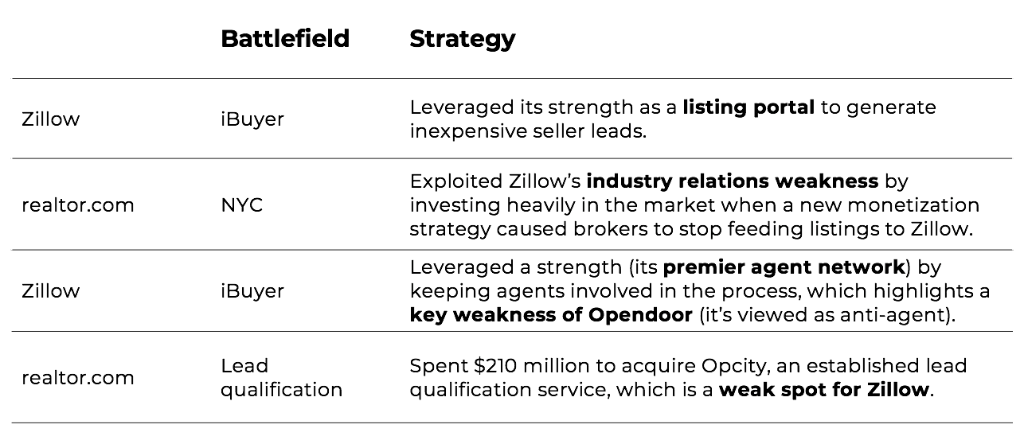

To illustrate this point further, the following chart looks at four examples of Zillow and realtor.com smartly leveraging their strengths and exploiting their competitor's weaknesses.

Less experienced strategists can be reactionary. They see a threat and attempt to counter it, on a battlefield where they are at a distinct disadvantage to a competitor. Keller Williams and Rocket Homes have done just this; choosing to do battle with Zillow on its home turf, where it is strong and they are weak.

Keller Williams and Rocket Homes

Zillow's strength lies in its massive consumer reach through its search portal. This business benefits from strong network effects and has a wide moat to protect it from competition.

Keller Williams is building a new consumer-facing app to "compete directly with search giants like Zillow and Redfin." Rocket Homes is launching a portal to "rival Zillow," which will "let consumers search for homes and apply for loans."

In their efforts build end-to-end homebuying platforms, both businesses have decided to go from positions of strength (mortgages and agent reach) to ones of weakness (consumer listing portal). It's the most difficult battle possible.

What Rocket Homes and Keller Williams are missing in their end-to-end platforms -- the consumer search portal -- is nearly impossible to deliver because of Zillow's dominance and the power of network effects. There's a certain futility in going after Zillow (or Facebook, or Ebay, or Craigslist).

Strategic implications

Keller Williams and Rocket Homes (part of Quicken Loans), are both incredibly large and powerful businesses; Keller Williams has the largest network of agents, and Quicken Loans is the largest retail lender in the U.S. But in the changing world of real estate, they aren't playing to their strengths.

All businesses should know their strengths. Deeply understand your competitive advantage and what value you offer -- and focus on that.

By going directly after Zillow, Keller Williams and Rocket Homes demonstrate a fundamental misunderstanding of the power of network effects. There's simply no purpose for these new consumer portals to exist, because they don't meaningfully benefit consumers.

In the accelerating race to build end-to-end real estate ecosystems, businesses should focus on leveraging their strengths to gain advantage over competitors and deliver true value to consumers.

Zillow, Opendoor, and controlling the consumer journey

/Last week I conducted the iBuyer Intelligence Briefing -- a conference call on the latest iBuyer news, trends, and insights -- with listeners from around the world.

After the call, one particular question lingered: Which part of the industry controls the starting point of the real estate transaction, portals or iBuyers? Who has the advantage, and what are the implications for iBuyers?

Zillow's lead generation machine

Zillow announced its Zillow Offers program in Phoenix earlier this year, and started buying houses in May. It is heavily promoting the program across its site. While looking in the Phoenix market, a prominent message is displayed on all active for sale listings.

And if a visitor looks at an off-market listing (like their own home), this is the call-out at the top of the listing.

In its latest quarterly results, Zillow revealed how effective the promotion was: "Since launch, we have received more than 10,000 offer requests from potential sellers." And: "...in Phoenix, for example, we are seeing about 15% of all dollar value that's being sold in Phoenix any given month." That translates to about 1,600 offer requests per month.

Opendoor is on record saying that more than "one in two sellers who received an Opendoor offer" will accept it. It's currently buying around 300 houses per month in Phoenix, so that's about 600 offers made per month.

There's a difference between an offer being requested, and an offer being made. What's clear, though, is that Zillow is generating a massive amount of offer requests each month, at volumes that rival (and exceed) Opendoor.

Most importantly, Zillow's leads are coming with zero incremental customer acquisition cost, while Opendoor and other iBuyers must advertise directly to consumers to generate leads.

The Zillow effect

The ultimate question is whether Zillow's entry into the market is having an effect on Opendoor. Is Zillow soaking up demand from consumers, to the detriment of Opendoor?

The chart above shows a clear picture: the number of homes that Opendoor is purchasing in Phoenix has plateaued. But there are two possible explanations for what's going on:

Zillow is having an effect on Opendoor's traction in Phoenix by soaking up consumer demand.

Opendoor is slowing its buying activity for other reasons (we've seen this before).

It's too early to say if Zillow is having a direct effect on Opendoor's business in Phoenix. Opendoor may slow its buying activity for a variety of other reasons, namely a potential market slowdown.

But what's clear is the leading position Zillow holds in the consumer journey and its massive reach give it a competitive advantage in acquiring customers -- which has long-term consequences.

Strategic implications

Back in February, I wrote the following: "The most logical response from a major player such as Realogy or Keller Williams would be to launch their own iBuyer program." Which is exactly what happened last week. More competition is coming to the market.

As incumbents, portals, and other new entrants enter the iBuyer market, they have the potential to soak up consumer demand and adversely effect Opendoor's business.

But for Zillow in particular, the evidence is clear: Real estate portals are in pole position to capture consumer demand for iBuying services, because they are at the start of the consumer journey. Will other global portals follow Zillow's lead?

Zillow will beat its Q3 homes revenue guidance

/With September wrapping up, we can look at the latest iBuyer numbers out of Phoenix and see how Zillow is doing.

Why it matters: Based on the data in Phoenix alone, Zillow will beat its Homes revenue guidance of $2 - $7 million. But other indicators, including a lower-than-expected margin and higher purchase prices, are worth watching.

Q3 Revenue beat

During its last earnings results, Zillow provided Q3 revenue guidance for its Homes unit of $2 - $7 million. Based on our proprietary data set for Phoenix, Zillow sold 30 properties in Q3 for $9.3 million in revenue. So in Phoenix alone, Zillow will beat its revenue guidance.

Thirty sales over three months is a modest amount. By comparison, Opendoor sold 26x that number in the same period. Zillow is clearly still in its ramp-up period and has some ways to go.

This result highlights a few other observations:

Guidance is hard. Zillow is still finding its way in this new endeavor, and is having to constantly readjust its assumptions. It’s a positive sign, but clearly highlights how new to this business Zillow is.

Zillow's full-year revenue guidance of $20 - $40 million in Homes revenue is achievable (it simply needs to sell the same number of houses in Q4 to hit the low end of that range), but a lot depends on traction in other markets. I would expect Zillow to revise this guidance during the next earnings call.

Buying momentum up

In Phoenix, Zillow continues to expand its operations on a month-to-month basis. The number of homes purchased is increasing by about 40% month-on-month — to over 60 in September. By comparison, Opendoor is buying around 5x as many houses in that same period (solely in Phoenix). Zillow is clearly serious and committed to this new initiative.

Unsold inventory

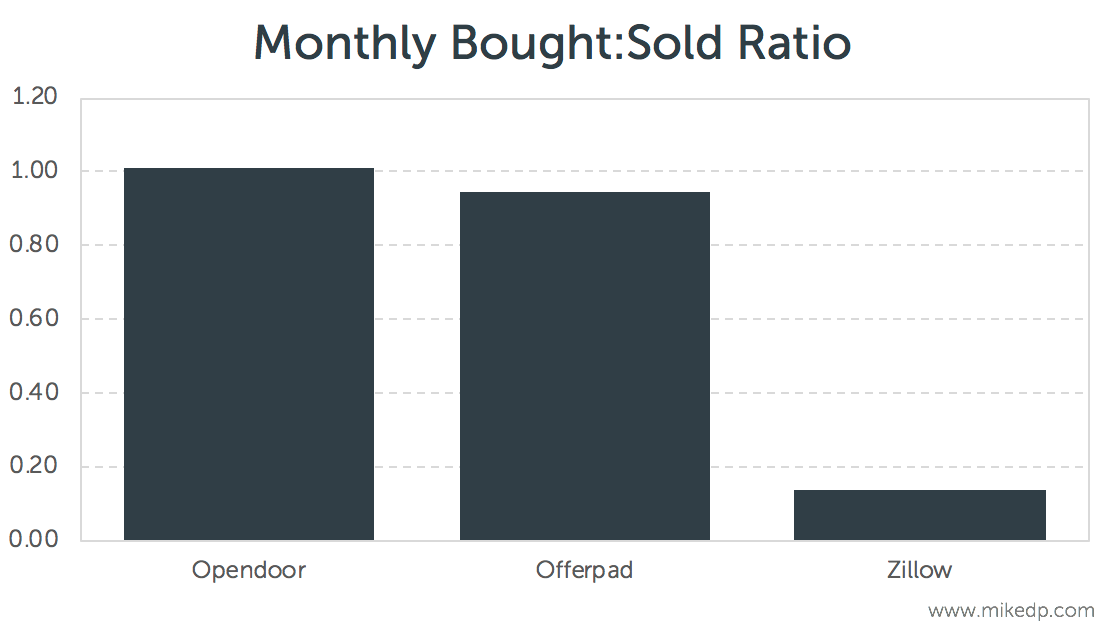

One of the potentially worrying indicators, however, is the amount of unsold inventory Zillow has in Phoenix. While the number of properties it is buying is increasing, the number sold is low.

To-date, Zillow has purchased over 150 properties and has sold 30.

In September, the ratio of homes bought to homes sold is 0.14 — down from 0.34 in August. Comparatively, that ratio for Opendoor is 1.01 and 0.95 for Offerpad.

Clearly Zillow is still ramping up its operations so it’s natural to expect a lag between buying and selling properties. But even accounting for a 90 day holding time window, the September number should have been larger (I would have expected a buy:sell ratio closer to 0.50). All eyes are on October.

There are a number of other interesting indicators worth watching:

A lower-than-expected margin (the difference between what Zillow buys and sells a house for).

A median purchase price that is materially higher than its iBuyer peers (but is starting to drop).

About the author: Mike DelPrete (email me)

Mike is a global real estate tech strategist, and a scholar-in-residence at the University of Colorado Boulder. He is internationally recognized as an expert and thought-leader in real estate tech. His evidence-based analysis is widely read by global leaders, and he is a sought-after strategy and new ventures consultant. His research and insights have featured in the New York Times, Wall Street Journal, Financial Times, and The Economist.

Latest analysis

All Articles