The Redfin Experiment is Over

With its acquisition by Rocket, Redfin’s saga as an independent company is coming to a close.

Why it matters: Launched in 2002, Redfin could be considered the original real estate disruptor, featuring discounted commissions, employed agents, and innovative technology – but the business model just never clicked.

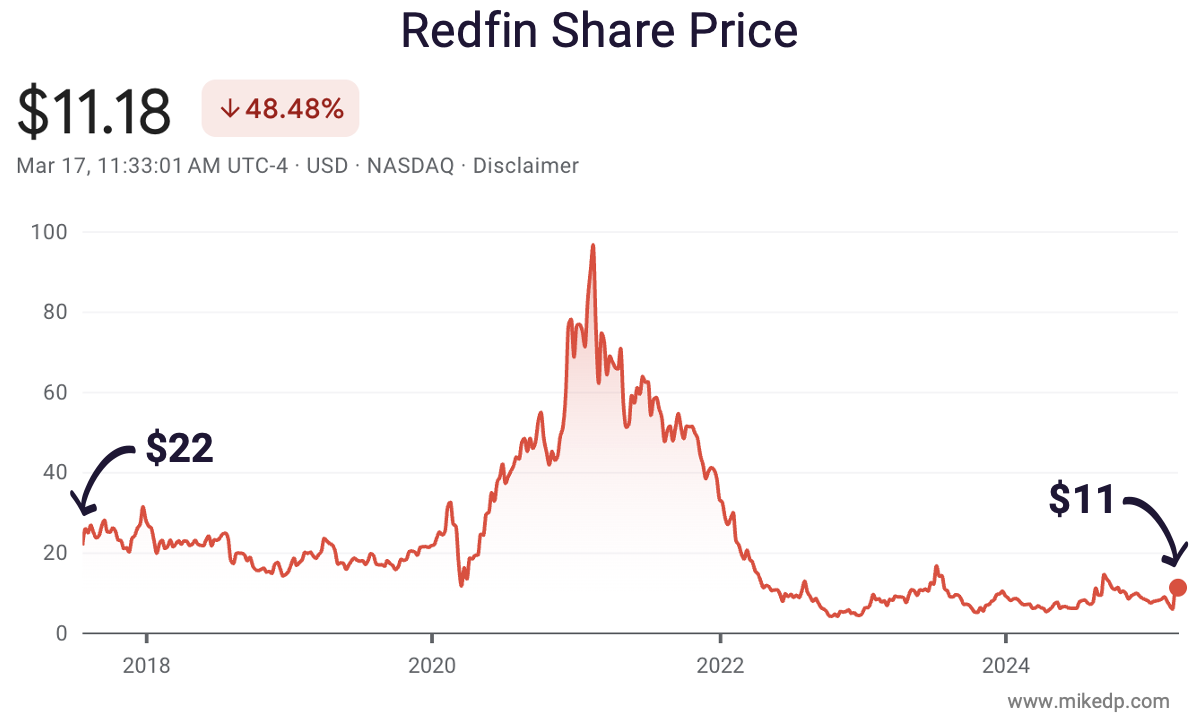

Redfin was rarely profitable, accumulated a large debt load, and was acquired for the same value as when it went public over seven years ago.

After its first day of trading as a public company in 2017, Redfin was valued at $1.73 billion – just shy of its acquisition price of $1.75 billion seven years later.

Yes, but: After Redfin’s first day of trading in 2017 each share was valued at $21.72, significantly higher than Rocket’s acquisition offer of $12.50 per share.

If you owned $100 of Redfin shares in 2017, they would be worth $58 today – a decline of 42 percent (due to dilution – it’s a thing!).

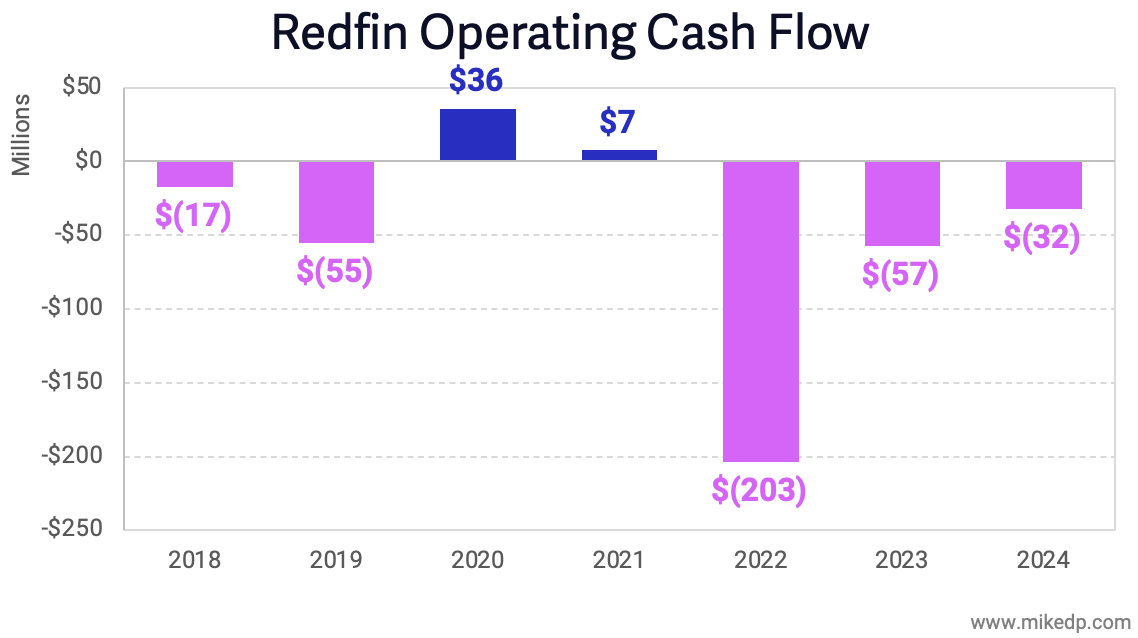

Redfin was never really profitable: Operating Cash flow, which measures how much cash the business generates, is a good corollary for profitability.

Since its IPO, Redfin had two profitable years vs. five unprofitable ones, for a combined loss of $368 million (again, this is actual cash flow and not “net loss” which includes non-cash expenses like stock-based compensation).

Redfin innovated in so many areas, from agent compensation to groundbreaking tech products, but at the end of the day it just didn’t make money.

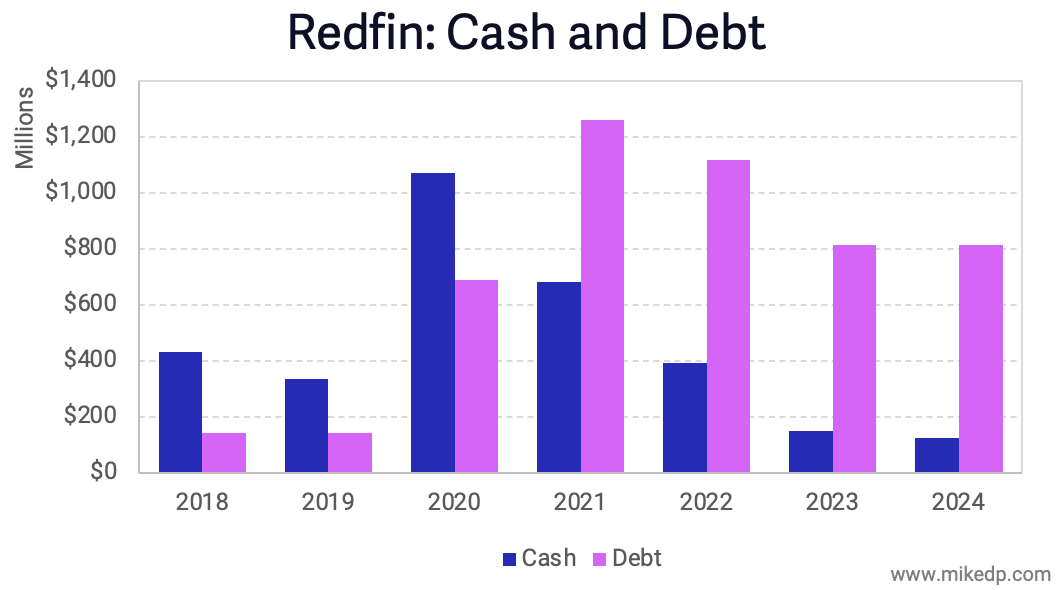

Not only is Redfin consistently unprofitable, but it has a high debt load – $815 million – with steadily dwindling cash reserves of just $125 million at the end of 2024.

Much of that debt, totaling over $1.2 billion by the end of 2021, was used to fund a pair of expensive acquisitions.

Redfin acquired Rentpath for $608 million in 2021, and Bay Equity Home Loans for $138 million in 2022.

It’s fair to say the acquisitions didn’t pan out as expected.

Redfin recently announced a deal that effectively outsourced its rentals business to Zillow for $100 million.

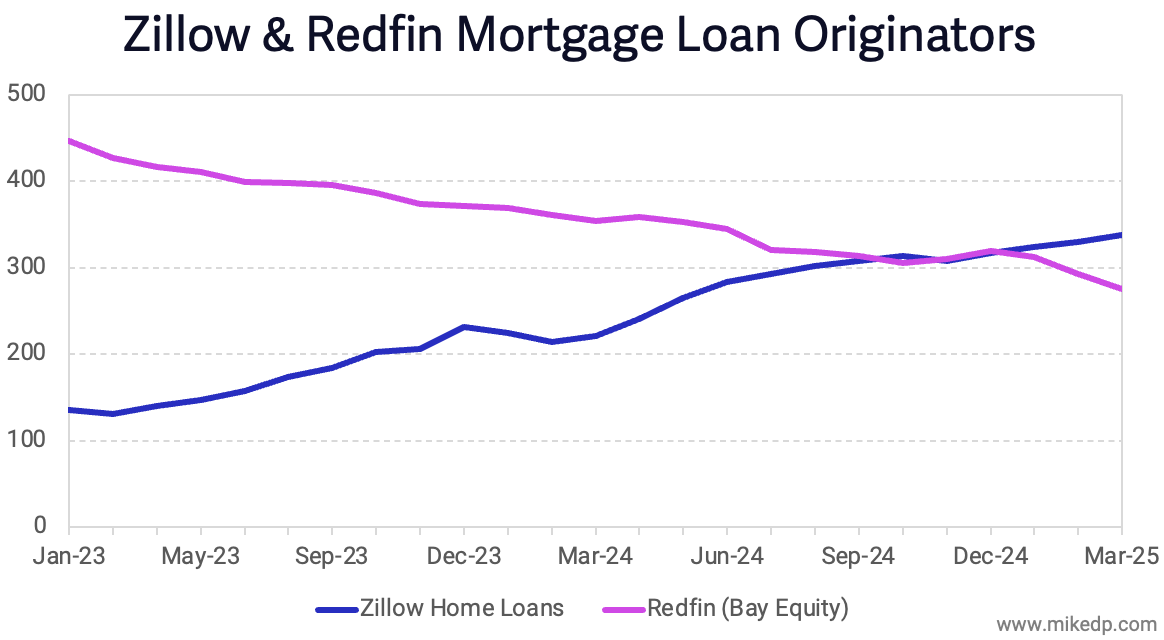

And in contrast to Zillow’s growing mortgage business, Redfin had to cut costs; its mortgage headcount declined from over 450 mortgage loan officers in 2023 to 275 in March 2025.

Real estate disruptors have a tendency to “go native” and, over time, end up looking more and more like the companies they were originally trying to disrupt.

It happened with iBuyers, with the now-defunct REX, and with Redfin, as the company slowly pivoted closer and closer to a traditional brokerage.

This Vox article from 2015 says it best: “Redfin set out to change real estate. Then real estate changed Redfin.”

The bottom line: Back in 2023 I said, “...it appears that Redfin is overstretched with limited resources and up against well-funded competitors…this is a galvanizing moment for the business; one way or another, something has to change.” Well, something did.

Redfin tried to do a lot: web portal, brokerage, iBuying, mortgage, rentals, title insurance, and more – with just one of those categories being more than enough to occupy a company full time.

In the end, it might be that lack of disciplined focus that prevented Redfin’s success – plus a lack of resource and scale – which the company now has after its acquisition by Rocket.