The Business Case for Exclusive Inventory

/

Brokerages and agents have clear incentives to promote exclusive inventory, a strategy that could significantly reshape power dynamics across the industry.

Why it matters: Understanding the motivations surrounding exclusive inventory is critical to predicting the direction this battle will take – and why brokerages like Compass are pushing it so hard.

This billboard mockup, used by Compass to explain the exclusive inventory strategy to its agents, succinctly sums up one key benefit.

The key phrase is “one week before any other site” – exclusive inventory is not exclusive forever; a better label might be “pre-marketing.”

The typical Compass exclusive is off-market for 2–3 weeks, with 94 percent of these listings eventually appearing on, and selling through, the MLS.

This pre-marketing period is akin to a restaurant soft opening – that’s a test run held before the grand opening, where a select group of guests try the restaurant and provide feedback, allowing it to fine-tune operations and menu before opening to the public.

For brokerages like Compass, providing access to exclusive listings helps to attract and retain agents, and any leads that come directly through the brokerage website could be monetized in-house rather than through a portal.

For agents, access to off-market listings is a very tangible way to provide and demonstrate value to potential buyers – and is a key differentiator to secure more clients.

The following chart shows the potential revenue benefit (after commissions are paid to agents) to Compass for every 100 agents recruited, closed compass.com website leads, and double-ended deals.

These estimates are based on the following assumptions: average sale price of $1.06M (Compass FY24), average agent production of 6.1 transactions per year (Compass FY24), average commission of 3 percent, website lead referral fee of 35 percent, and an 82 percent agent commission split (Compass FY24).

In aggregate and at scale, these benefits could be worth $50–$100 million or more in additional revenue per year.

Another financial benefit comes from using access to a large pool of exclusive inventory – a major value to agents – to gradually shift commission splits in the brokerage’s favor.

Compass’s average commission split is 82/18 (82 percent to the agent, 18 percent to the brokerage).

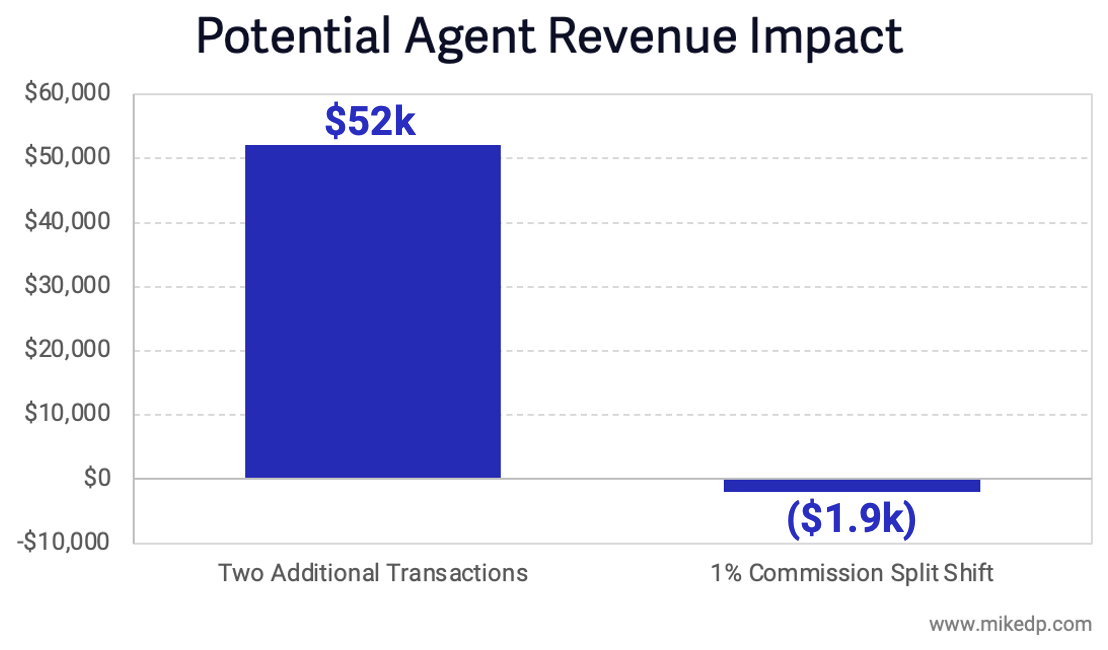

Shifting that just one percentage point would be worth $56 million to Compass while, on average, costing an agent $1,940 per year (using the same assumptions above).

For an individual agent, being able to secure two additional transactions per year (buy side or sell side) through access to exclusive inventory would, on average, yield $52k in additional income.

Three additional transactions would yield $78k, which, in either case, far outweighs the $1,940 an agent might give up from a one percent reduction in their commission split.

It’s really a financial win-win for agents and brokerages.

The big question: Is exclusive inventory, or a pre-marketing “soft opening,” good for consumers? Far be it for one author to make that determination for the totality of sellers in the United States.

At the end of the day, homesellers are choosing whether it’s good for them or not, based on their particular circumstances and the benefits of the program – and in the case of Compass, 55 percent of new listings opted in to the program in February.

Compass is not alone; behind the pro-consumer headlines, nearly everyone – from NAR to MLSs, from big and small brokerages to the portals – has a financial motivation to fight for for the expansion or contraction of exclusive inventory.