Zillow's billion dollar seller lead opportunity

/Last week, Zillow announced its latest financial results, and the stock dropped 25 percent (losing $2 billion in value). But the story everyone is missing is the Zillow Offers iBuying business, and the huge potential of seller leads.

Why it matters: Last week I was quoted on MarketWatch saying, “If you’re thinking about Zillow doing iBuying and you’re not thinking about seller leads, you’re thinking about it the wrong way.” Seller leads are the real billion dollar opportunity.

Slowing premier agent growth

Here's the reason why Zillow's stock tanked 25 percent last week, in one chart:

Zillow's premier agent program accounts for over 70 percent of its revenue, or nearly $1 billion. Growth is slowing down. I'm not sure why this surprised anyone on Wall Street; I've been writing about it since early this year (Zillow's revenue growth slows and Zillow's strategic shift to iBuying and mortgages). I believe it's the primary reason Zillow has aggressively expanded into adjacent businesses.

The value of seller leads

Zillow's iBuyer business continues to grow, and the latest results crystalize the opportunity in seller leads.

Zillow says that since launch, nearly 20,000 homeowners have taken direct action on its platform to sell their home. Of those, it has purchased just about 1 percent of homes (around 200). That leaves about 19,800 leads who remain interested in selling their homes.

If Zillow simply sold those leads at $100 a pop, they're worth nearly $2 million.

But the real opportunity is giving those leads to premier agents in exchange for an industry-standard referral fee, about 1 percent, if the property sells (similar to the Opcity business model).

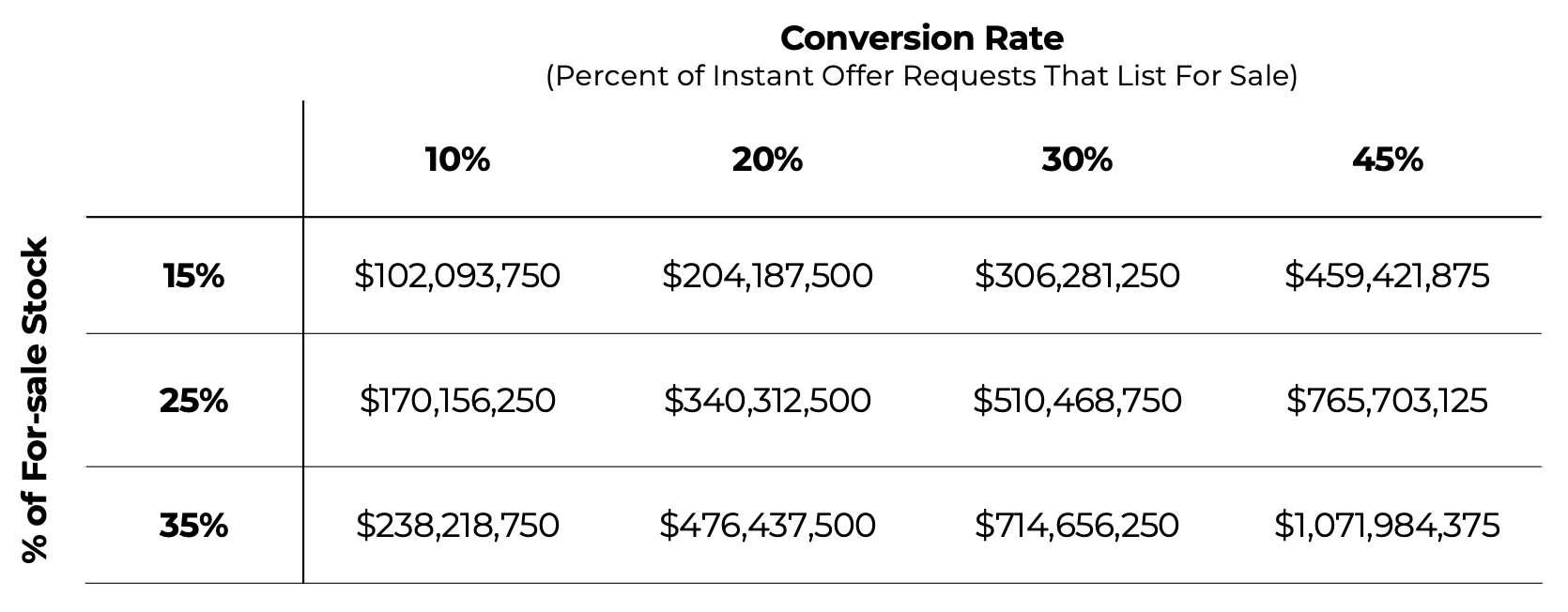

Here's the kicker: Zillow claims about 45 percent of consumers that go through the Zillow Offers funnel end up listing their home. That's a high conversion rate reflective of a high intent to sell; about 10 times higher than Opcity's conversion rate.

Assuming a 1 percent referral fee, a $250,000 home, and a conversion rate of 45 percent, those 19,800 leads are worth $22 million in revenue to Zillow, almost all profit.

Compare that to the estimated profit of its iBuyer business (1.5 percent net profit), which, on 200 houses, is $750,000. The value of the seller leads is worth almost 30 times the profit from flipping houses!

Total addressable market

Zillow says that based on its current purchase criteria, if Zillow Offers were available in the top 200 metro areas in the U.S., sellers of nearly half of the homes sold in 2017 across the entire nation would have been eligible to receive offers from it to buy their home directly. That equates to around 2.75 million homes annually.

Last quarter, Zillow said that it received offer requests from around 15 percent of the total for-sale stock in the Phoenix market. Interestingly, that number increased to 25 percent in September and 35 percent in October. That's a reflection of the strong lead generation power of Zillow Offers across its various web properties.

Based on these numbers, if Zillow goes national (200 metro areas) and sees 35 percent of the for-sale stock, it would receive 962,500 offer requests each year.

The billion dollar opportunity

Taking the latest numbers, which have been validated to the tune of 20,000 offer requests over five months in two markets, the total opportunity becomes clear with a national rollout.

Seller leads can be a billion dollar business for Zillow if you believe the current numbers. Even if a national conversion rate is lower, or the % of for-sale stock fluctuates, it's still worth several hundred million dollars in revenue annually.

Should Zillow even buy houses?

Given the value of the seller leads, should Zillow even be in the business of buying houses? Yes, if it wants a credible product for consumers. The real question is: What proportion of houses should Zillow actually buy?

Zillow's "big picture" is 5 percent national market share, which equates to buying around 10 percent of all offer requests (it is currently buying around 1 percent of offer requests). At a 1.5 percent net margin, that's around $1 billion in profit.

But to reach that scale, Zillow would need to spend $68 billion to purchase 275,000 houses annually. Assuming an average holding time of 90 days, it would need a credit line of $17 billion to fund the effort. Big numbers.

A more realistic target would be to only purchase around 1 percent of requests. Nationally, that would be 27,500 homes, which is only around double what Opendoor is currently doing, so it's feasible.

In any case, the point is clear: Zillow doesn't need to actually buy and sell a lot of houses for this model to generate significant profits for the company in a national rollout.

Strategic implications

Zillow is a lead generation machine, and its recent foray into iBuying is no exception.

If you're in the industry and your value proposition to agents is seller lead generation, there's a new game in town. Zillow will be able to generate a massive volume of seller leads with higher intent than almost any other source. If successful, this will have significant implications across the industry.

Further analysis

If you're looking to dive deeper into the world of iBuyers, consider the following:

iBuyer Business Model Overview and Analysis: all of my free research and reports on the iBuyer space.

iBuyer Intelligence Briefing (Recording): a 60-minute conference call I conducted on the latest iBuyer news, key insights, and strategic implications for the real estate industry.

Phoenix iBuyer Report: the only source for accurate, timely iBuyer market data for Phoenix. Available as a monthly subscription.