REA Group, Domain, and the non-battle for top spot

/It's earnings season! In the past week, a number of portals announced their financial results, including REA Group and Domain, the two top Australian portals.

Why it matters: The numbers reveal interesting trends and insights, significantly around the difficulty of building meaningful adjacent businesses, and the non-battle between the #1 and #2 players in various markets.

Adjacent businesses are tough

Like many portals worldwide, REA Group and Domain each launched adjacent businesses, with goals to expand along more of the transaction, reduce consumer friction, and capture more revenue.

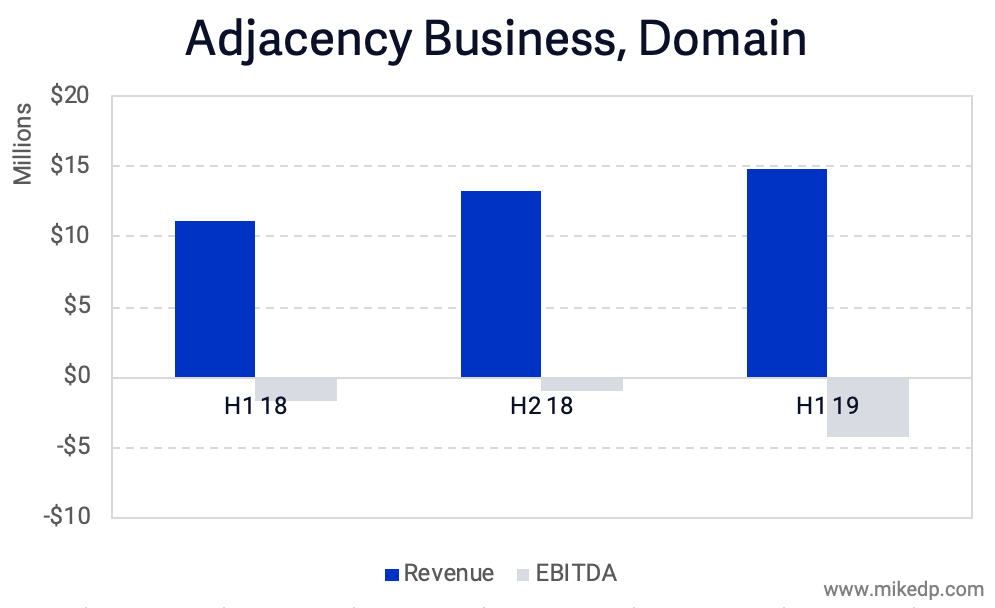

But as I've written before, the businesses have very different strategies. REA Group acquired a majority stake in an existing mortgage broking business, while Domain launched a number of joint ventures and partnerships. Different strategies, different outcomes.

REA's finance business continues to chug along, building revenue and generating meaningful earnings ($5.8 million EBITDA over the last six months).

By comparison, Domain's adjacent businesses (finance, insurance, and utility switching) generate similar revenues but with continued -- and mounting -- losses. The latest six months show a loss of $4.3 million.

REA's strategy is delivering a positive financial impact, while Domain's businesses are still in a heavy investment phase after more than a year.

The "battle" between #1 and #2

The battle between the #1 and #2 portal in each market is fascinating, and Australia is no exception.

One metric to compare portals is overall revenue generation. In general, the #2 portal generates between 25 and 40 percent the revenue of the leader (read my portal report), and that number doesn't fluctuate over time. In fact, in the case of REA Group and Domain, the leader is growing faster than the number two.

Domain is the underdog in Australia, and the evidence suggests it will remain that way. Overall situational awareness is important: It would be a mistake to assume Domain will overtake REA in any capacity.

U.K. portal wars -- what's changing?

Along the same lines, the real estate portals in the U.K. recently released traffic figures for the start of the year. It offers yet another fascinating glimpse into the competitive tension between top players -- and the complete lack of movement.

The figures released are for January 2019. And while the absolute numbers are generally rubbish, it's the comparison between portals and the year-on-year growth that's insightful.

Rightmove's numbers have hardly changed, and the delta between the number one and two is still the same. For all the investment on product, marketing, and inventory -- the all important consumer habits haven't shifted.

The variable, however, is the upstart portal OnTheMarket (read my past analysis). OTM has raised over £30m and is aggressively spending on marketing in order to drive traffic to its site. Its traffic has doubled since last year -- but does it matter?

For all of the tens-of-millions of pounds spent to build an alternative to the established portals, what impact is it having after launching four years ago? Zoopla's traffic is marginally down, but it reports that leads are up over 30 percent. The top two portals are equally and exactly as dominant as they were a year ago.

Strategic implications

There are a number of key takeaways for portals around the world:

Launching successful adjacent businesses is hard. It takes an incredible amount of investment, and there are a variety of execution strategies.

The evidence doesn't suggest that the #2 portal can overtake the leader -- let alone make a dent in its leadership position. It's not a horse race; it's static trench warfare.

Trying to launch a new portal and compete against the leaders is at best expensive, and at worst futile. Consumer habits are hard to change.