Purplebricks’ Market Share Ceiling

/Purplebricks’ H1 2020 financial results highlight a business whose growth has clearly plateaued and reached maturity in the U.K. The company appears to have reached peak efficiency, putting a ceiling on its future growth prospects.

Financials: Profitable, But No Longer Growing

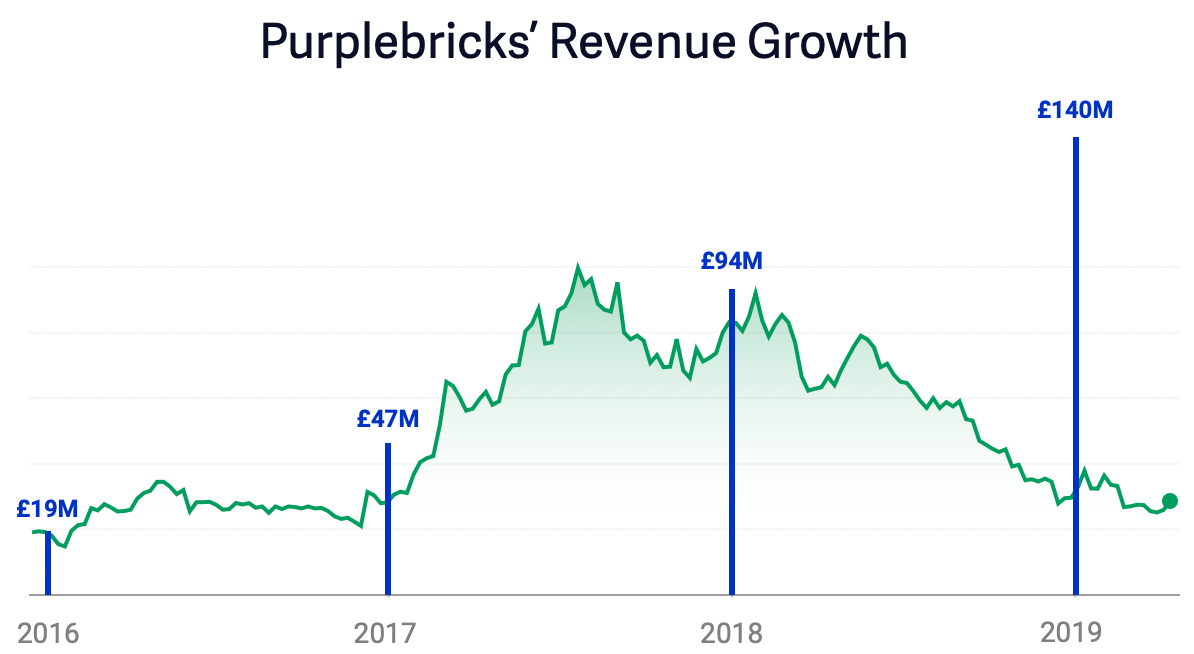

Purplebricks’ revenue growth in the U.K. has effectively stopped. Total revenue is down from the same six month period last year, and the overall growth picture has gone from growth in 2018 to a plateau in 2019 and 2020.

Purplebricks’ U.K. business is still profitable, which is becoming a rarity in the world of real estate tech brokerages. Other high-flying overseas disruptors, like Redfin, Compass, and Opendoor — which have raised billions of dollars and are grabbing market share from traditional incumbents — are all unprofitable.

The fundamentals of the Purplebricks business model are sound, with demonstrated profitability, but it has clearly hit a glass ceiling in terms of market share. Its number of customers, as measured by "instructions to sell," has remained flat over the past two and a half years.

Purplebricks remains a business that scales linearly based on money (marketing costs to acquire customers) and people (local property experts to service those customers).

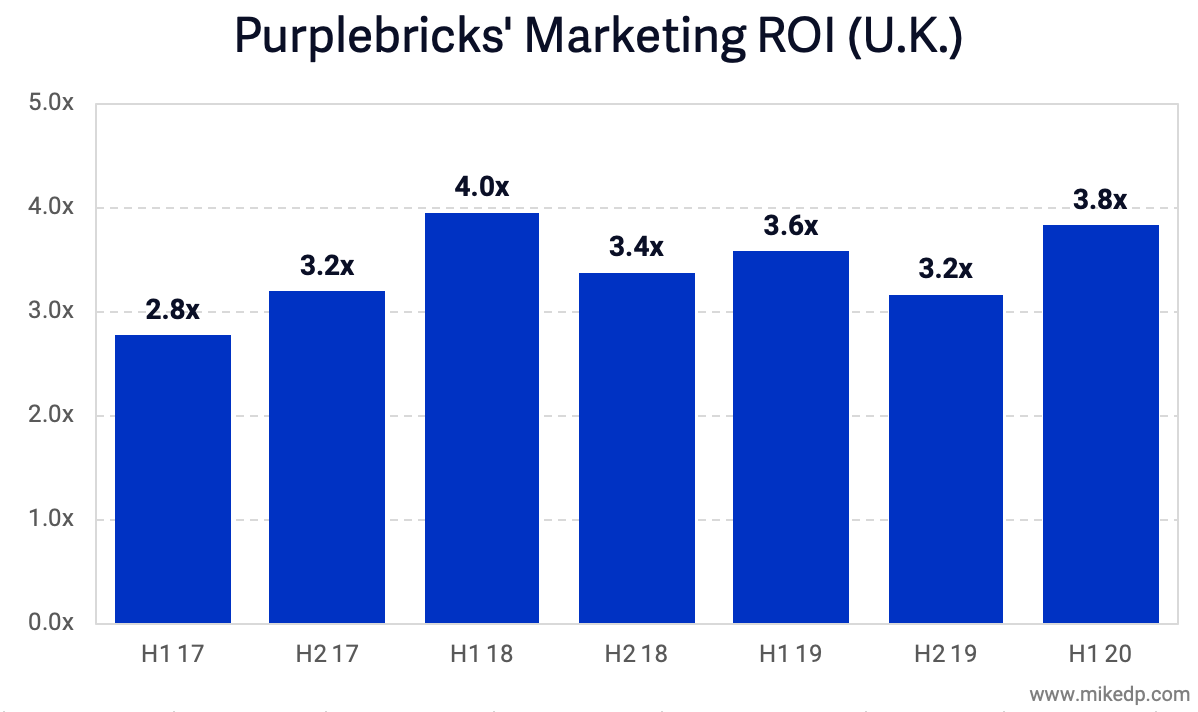

Marketing ROI

One key to the Purplebricks business model is efficient marketing spend at scale. On a positive note, its marketing return on investment (ROI) has bounced back up in the most recent six months. Each £1 invested in marketing returned £3.8 in revenue.

By way of comparison, Redfin had a marketing ROI of 9.8x in 2018 and 5.9x in the first nine months of 2019 — significantly higher than Purplebricks. This is a reflection of the value of Redfin’s popular consumer portal; having tens of millions of visitors browsing listings helps the brokerage acquire customers at a relatively low cost. (Last week I wrote about the difficulty — and incredible competitive advantage — in building a large consumer audience.)

Overall customer acquisition cost (CAC) has also remained relatively flat, at around £375 per customer. This number really hasn’t changed much in over three years. The small fluctuations suggest a business model that has reached peak efficiency for customer acquisition — again highlighting a limiting factor in growing market share.

Gross Margins

Purplebricks is a business with a novel operating model. It has managed to change how traditional estate agents are compensated, with a structure more similar to Uber than a traditional real estate brokerage. As a result, its gross margins, 64 percent, are top of the industry. (For more on this, check out Inside Compass — Part 5: Endgame.)

Industry Average: REAL Trends U.S. reporting, Redfin: Brokerage Services Only, Compass: author's estimates.

Lessons Learned

I continue to use Purplebricks as a case study of successful disruption in my university course on real estate tech. Going from an idea to the largest estate agent by market share in the U.K., with a profitable business model (in the U.K., at least), is impressive and worthy of study.

In the U.K., Purplebricks succeeded where every other hybrid agency failed: by scaling. While its competitors slowly went out of business while failing to demonstrate a path to profitability, Purplebricks — partially through sheer force of will and spending power — managed to scale to the point of profitability.

But while Purplebricks managed to cross that first chasm, it never really made it over the next one: becoming a platform. The business still scales linearly based on marketing spend and people; I've yet to see evidence to support a credible path to double-digit market share. In the U.K., this may be as big as the business can get — a high-water mark for the hybrid agency model.

{kind=link}