Zillow’s Most Interesting Product

/

In a year dominated by a confusing market, major advances in AI, and disruptors fighting for survival – Zillow has arguably released its most ambitious product since iBuying: Listing Showcase.

Why it matters: Listing Showcase represents a new business model – from pay-per-lead to pay-per-listing – which is aligned to how Zillow’s very profitable international peers monetize their market-leading positions.

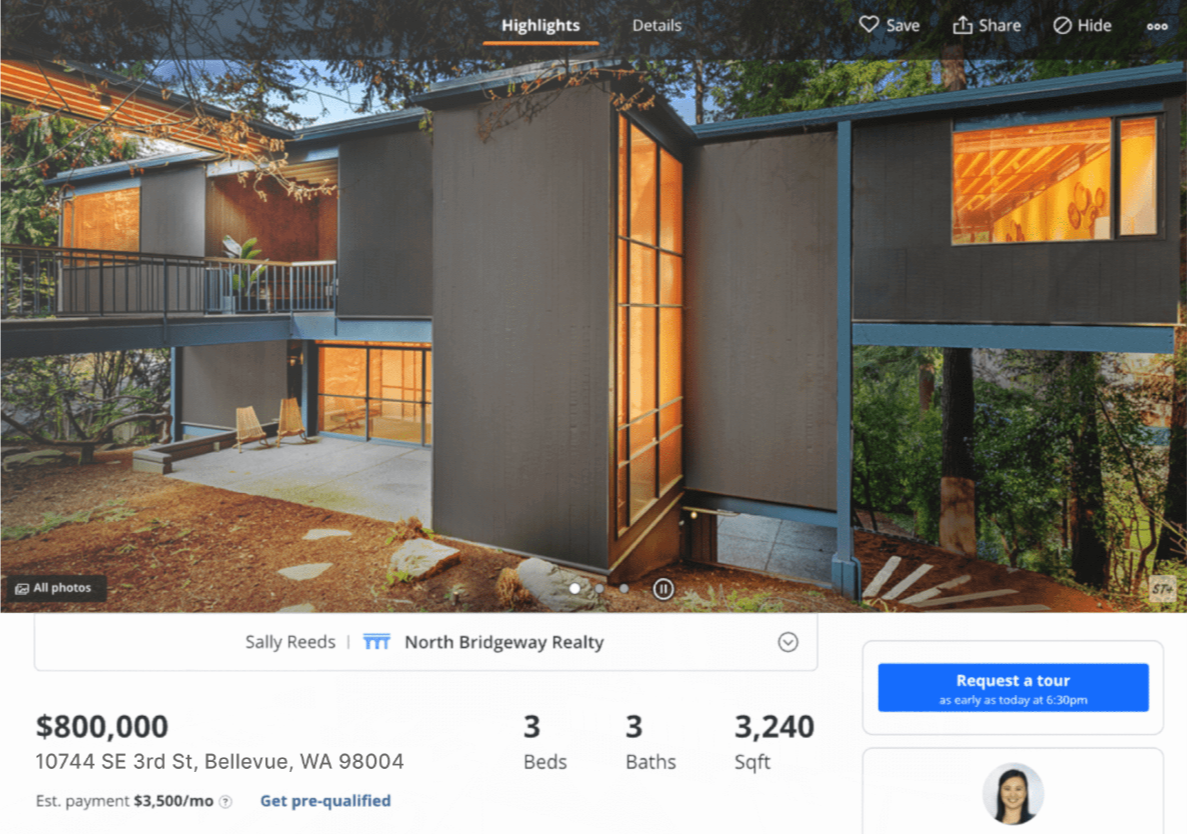

The Listing Showcase product promotes a specific listing with larger photos, enhanced agent branding, and premium placement in search results.

It’s also exclusive in each market, providing participating agents a unique advantage over other agents (“only my listings are enhanced in this market, making your property stand out”).

The result is a high profile listing with strong agent branding, ideally leading to more seller leads for partner agents.

Dig deeper: For years, seller leads have been the mythical holy grail of online real estate – incredibly valuable, but very difficult to generate at scale.

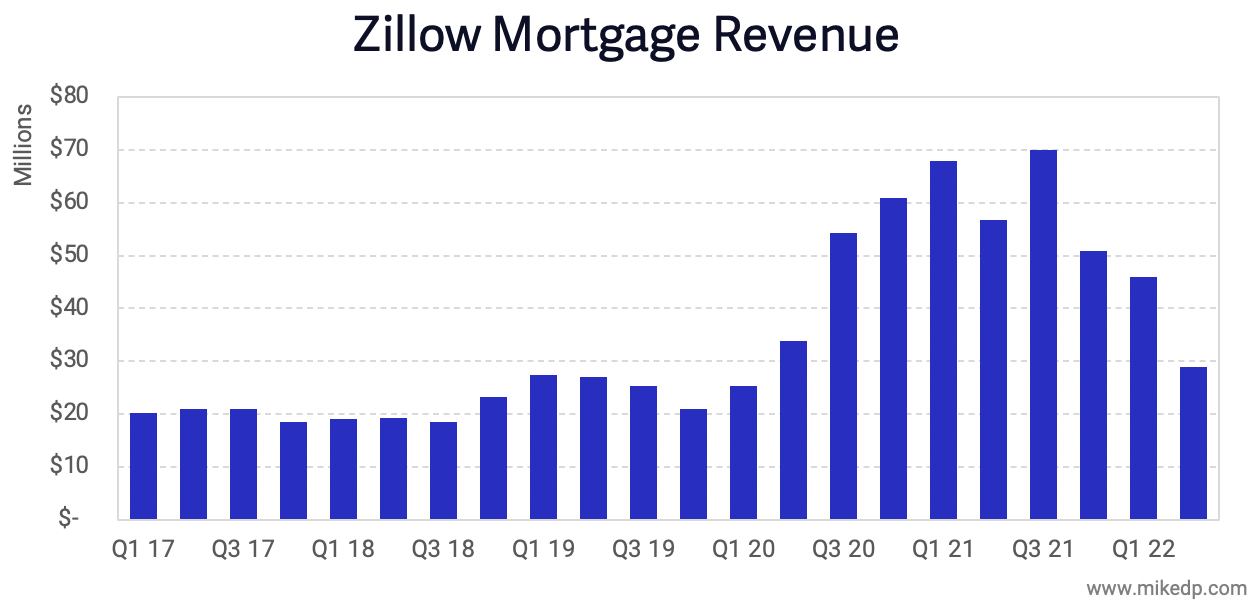

One surprise of the last five years was iBuying, which despite its challenges, turned out to be a great way to generate high quality, high intent seller leads (read more: Zillow's billion dollar seller lead opportunity).

Before it was shut down, Zillow Offers was generating tens of thousands of valuable seller leads per month.

Like its overseas peers, Zillow is using the concept of scarcity to increase the value of Listing Showcase; if it were available to any agent willing to pay, it would confer no unique advantage – but offered on an exclusive basis, the value becomes exponentially higher.

Without an MLS, nearly all international portals charge agents (or home sellers) on a pay-per-listing basis, with multiple tiers of enhanced exposure.

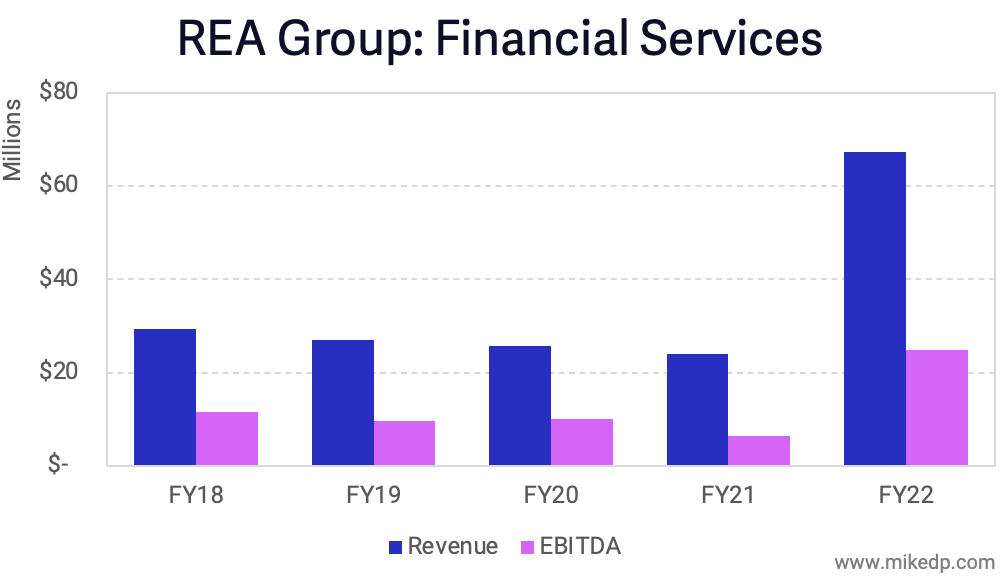

Australia’s REA Group is masterful in the art of premium listings, which always include larger photos, premium placement in search results, and enhanced agent branding – all of which are features of Zillow’s Listing Showcase.

Yes, but: By only promoting the listing agent, Listing Showcase will cannibalize Zillow’s existing buyer lead business – but that’s not necessarily a bad thing.

Listing Showcase is a hedge against any potential impact from the various lawsuits that may restrict or change buyer agent commissions.

It also neutralizes the threat of CoStar's "your listing, your lead" product offering.

The bottom line: Listing Showcase is a serious, credible attempt by Zillow to expand its business from selling leads to selling exposure.

Modeled on its international peers, Listing Showcase has the hallmarks of a classic pay-to-play premium product, which, on a per listing basis, is a significant endeavor for the company.

At its best, it’s a potential premium revenue stream that’s good for agents (the ones that pay), consumers, and Zillow's bottom line.