Zillow’s Transition to “Super App” Driving Revenue Growth

/

Zillow’s latest momentum is a manifestation of its strategy to diversify revenue across the transaction as it transitions from a lead gen platform to a housing “super app.”

Why it matters: As Zillow scales new revenue streams, including Zillow Home Loans, Rentals, ShowingTime+, and Seller Solutions, it is planting important seeds for its next phase of growth.

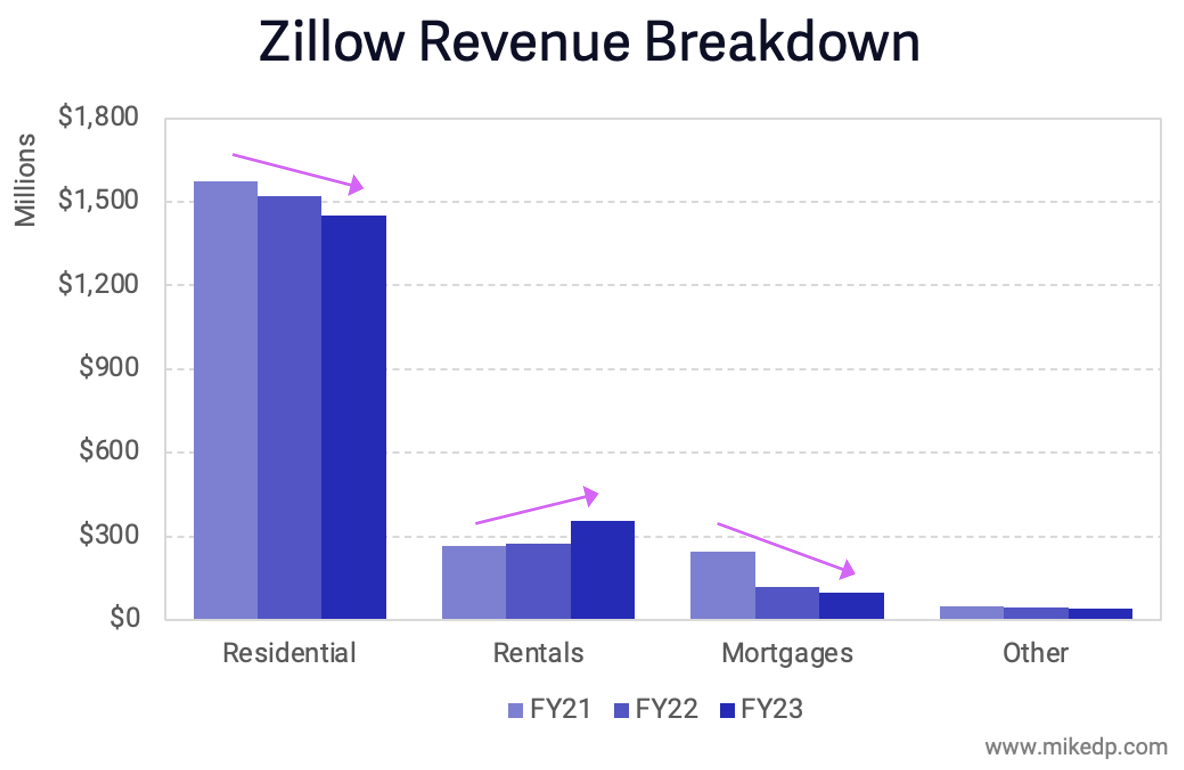

Context: After a pandemic bump, Zillow’s overall revenue declined and has remained flat since 2021 – during one of the worst real estate markets ever recorded.

Over a challenging two years, Zillow’s residential and mortgage businesses have shrunk (on par with the declining market), while its rentals business has ticked up from strong organic growth.

Even with flat revenue, Zillow has significantly outperformed the market during this period, with the magnitude dependent on whether you consider Zillow a lead generation platform or a housing “super app.”

While revenue growth at Zillow, the lead generation platform, has slightly outperformed the market, revenue growth at Zillow, the housing super app, is outperforming at a much higher rate.

This is a result of new products and services that are generating additional revenue across more of the transaction.

Dig deeper: For years I’ve used the following framework to think about real estate portal growth strategy.

Zillow’s evolving strategy sees it getting closer to the real estate transaction (Zillow Flex and Zillow Home Loans) and expanding to more parts of the transaction (Mortgages, Rentals, Seller Services, Agent Tools).

Typically, services closer to the transaction are higher revenue, while services further from the transaction are higher margin and more scalable.

Zillow asserts that its strategy to grow transaction and revenue share is working.

The drivers of that growth – in its early enhanced markets – appear to be a combination of growing Zillow Home Loans, cycling out underperforming Flex teams, and launching new seller solutions (Listing Showcase and the Opendoor partnership).

Zillow’s mortgage business is growing, but, counter-intuitively, revenue is dropping as purchase volume nearly doubles.

This is a result of a shifting product mix – Zillow is funneling leads from its mortgage marketplace to fulfillment by Zillow Home Loans.

It’s shifting from an asset-light marketplace to an asset-heavier mortgage brokerage operation, with much higher revenue potential.

Last year I claimed that Listing Showcase was Zillow’s most interesting product, and now it’s probably Zillow’s most interesting slide in its investor presentation.

The mid-term revenue potential is spot on based on my earlier calculations, representing a significant revenue opportunity as a new, sell side product.

But the most interesting opportunity is long-term, where Listing Showcase could be rolled out as a mass market product for all agents.

What to watch: Zillow’s future growth aspirations hinge on a few key factors.

Expansion into 40 markets – as early “enhanced markets,” Atlanta and Phoenix are useful data points, but not necessarily representative of all 40 markets.

The last mile problem – Zillow remains completely dependent on local real estate agent teams to drive adoption of its new products.

Zillow Home Loans is driving revenue, but it’s unprofitable, lower-quality revenue – the business needs to demonstrate an ability to grow revenue faster than expenses.

The bottom line: Zillow is diversifying its revenue along the transaction – what it calls its super app – and is outperforming a depressed market.

Zillow will almost certainly miss its $5 billion in revenue by 2025 goal, but like many plans that were laid in early 2022, things have changed.

While early signs are promising in a few key markets, the path forward hinges on the stubborn realities of conversion rates, profitability, and – as always – partnering with agents.